Money laundering and terrorist financing are the global concerns. Due to the widespread use of technology and the global economy, it has become easier for criminals to set up shell companies and run their ill-motives. The article, ‘What is a shell company and how does it operate?’ throws light on the associated money laundering and terrorist financing risks and the modus operandi.

What Is a Shell Company

According to the meaning interpreted from the Cambridge English dictionary, a shell company is a legal entity that does not have any operations or own any assets but is used to hide a natural or legal person’s activities. In plain words, Shell Companies are those companies formed only to exist on paper but not have any real business operation to serve several legal as well as illegal purposes discussed further in this article.

Key Characteristics of a Shell Company

Shell Companies are often characterised by having a legal existence, but such an existence is not alive with the hustling bustling business with any real product or service, supply chains, real employees, and operational business with assets, liabilities, contracts, suppliers, and consumers. However, shell companies do have a bank account, often in a secrecy haven, complex layers of ownership, nominee accounts, and dummy employees or business transactions that exist only on paper to create an illusion of legitimacy.

Functions of a Shell Company

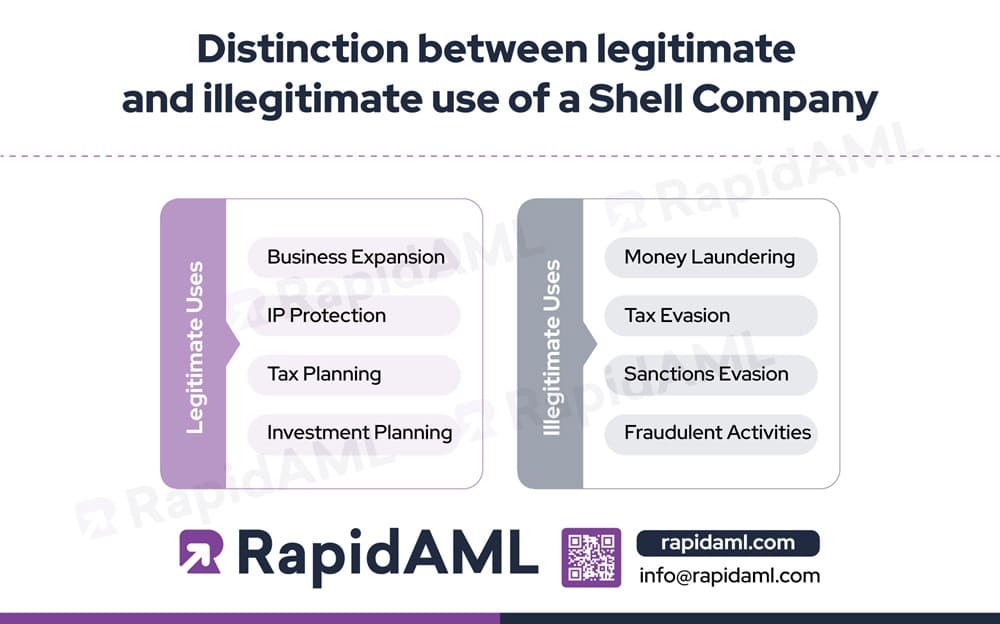

Every Shell Company’s function can be broadly divided into two categories, it may serve legitimate functions like:

- Business expansion

- IP protection

- Tax planning

- Investment planning

Or illegitimate functions like:

- Money laundering

- Tax evasion

- Sanctions evasion

- Fraudulent activities

Not Every White Shirt Is Crisp Clean, The Dirt Might Be Hiding in the Collar

Just Because a Company Looks Legitimate Doesn’t Mean It’s Free from Hidden Risks, Check Beneath the Surface.

Distinction between Legitimate and Illegitimate Use of a Shell Company

Shell companies serve legal as well as illegal purposes due to their nature of being an entity that exists on paper but does not have operations or assets. The legally permissible and non-permissible uses of shell companies are expanded below.

Legitimate Uses:

- Business expansion: One of the most important uses of shell companies, making their use and formation popular, is business expansion. Companies make use of shell companies to access and enter new markets in foreign countries by forming entities in such jurisdictions. Doing so enables them to manoeuvre legal requirements and compliances in that country without having the current entity and its business operations interrupted in any manner. In simple words, shell companies act as vehicles to enter and smoothen international business operations.

- IP protection: Another use of shell companies is IP protection, meaning that individuals and businesses make use of shell companies to own and hold intellectual property rights such as patents for technology, medication, science, and so on. Using shell companies for IP protection works by creating a legal barrier in the form of the shell company between the individual or company to whom the IP right belongs, shielding them from subsequent legal liabilities that arise from holding such IP right through the shell company.In simple words, shell companies separate the actual IP owner and the legal obligation arising out of such IP by itself, becoming answerable for the IP. The beneficial owner of such a shell company is the real IP owner, who, to dilute their liability from the IP, creates a shell company and makes the shell company the owner of the IP, safeguarding their individual self from potential lawsuits or associated risks. Shell companies help IP owners such as individuals and companies with asset segregation and privacy benefits as the ownership structure of shell companies is usually shrouded with confidentiality. Shell companies also act as a strategic litigation mitigation tool to shield main businesses and rights from IP litigation risk.

- Tax planning: Legitimate tax planning measures, such as transfer pricing, etc., are usually facilitated by shell companies. Forming shell companies helps individuals and entities minimise tax liability by helping them diversify their profits and create transfer pricing agreements that help lower tax liability.

- Investment planning: Shell Companies are used by companies and high net worth individuals (HNIs)for investment planning as they are usually formed in tax haven countries to hold assets and act as a vehicle to manage investment portfolios. Such portfolios could have stocks, bonds, and various other financial instruments.

Illegitimate Uses:

- Money laundering: Money Laundering (ML), Terrorism Financing (TF), and Proliferation Financing (PF) are grievous threats to any economy, posing deadly consequences to the public at large. Shell Companies are misused extensively by money launderers, terrorists, and proliferation finance actors to move funds illegally and hold or store investments ready for mobilisation when needed. The international Anti Money Laundering (AML), Counter-Terrorism Financing (CTF), and Counter-Proliferation Financing (CPF) watchdog- Financial Action Task Force (FATF) gives recommendations and suggests as well as facilitates its member nations’ measures to curb ML, TF, and PF. Some of the examples of AML, CTF, and CPF legislations in force across major countries and their compliance requirements and technology-based prevention measures are discussed in the following articles:

- Tax evasion: Shell companies are extensively used for tax planning to the extent that many governments are now taking measures to prevent the misuse of shell entities for tax purposes. Examples of some of these legislations include:

- European Union: “Unshell Directive” also known as the “European Anti-Tax Avoidance Directive 3 (ATAD 3) Directive” is an upcoming EU Directive aimed to prevent the misuse of shell companies for tax evasion purposes.

- United Kingdom (UK): provisions of the Criminal Finances Act 2017

- United Arab Emirates (UAE): Federal Decree-Law (28) of 2022 on Tax Procedures, article 25.

- Australia: relevant provisions of Criminal Code Act 1995 against obtaining financial advantage by deception contained in divisions 134 and 135.

- India: The General Anti-Avoidance Rule (GAAR) rule under the Income Tax Act, 1961 of India and the provisions of the Indian Penal Code.

- Sanctions evasion: Shell Companies are extensively used by sanctioned individuals to avoid detection of their actual identities. Using Shell Companies helps sanctioned individuals or entities enter business relationships and conduct transactions behind a shell entity’s guise without disclosing their identity, which might be flagged while sanctions screening if they were to approach the regulated entity for business directly. Many regulators across the globe recommend that regulated entities make use of technology to detect and report sanctioned individuals. Our article on Elevate AML compliance with Name Screening Software explains how a name screening tool can help identify sanctioned individuals. Criminals, sanctioned individuals, and entities often resort to creating complex ownership structures by having multiple layers through a web of legal arrangements and shell organisations as beneficial owners or subsidiaries of other legal arrangements and shell organisations to obscure the ultimate beneficial ownership (UBOs). Regulated entities must strive to identify UBOs and maintain their registers for regulatory inspection and reporting to ensure adequate AML/CFT and CPF Compliance. The creation and use of nominee accounts are also done to evade sanctions detection by hiding the UBO identities.

- Fraudulent activities: Shell Companies, apart from other misuses, give rise to fraudulent activities conducted behind the garb of the Shell Company by criminals. One example is how billing and invoice-related fraud facilitates trade-based money laundering (TBML). Also, many Ponzi Schemes are run by fraudsters by using Shell Companies to loot unwitting people into investing in such schemes, whereby the time the people realise that they may have been defrauded, the fraudsters would have already escaped with their funds. Also, false invoicing/re-invoicing schemes are used to evade taxes by creating and claiming fraudulent deductions

Structure of a Shell Company

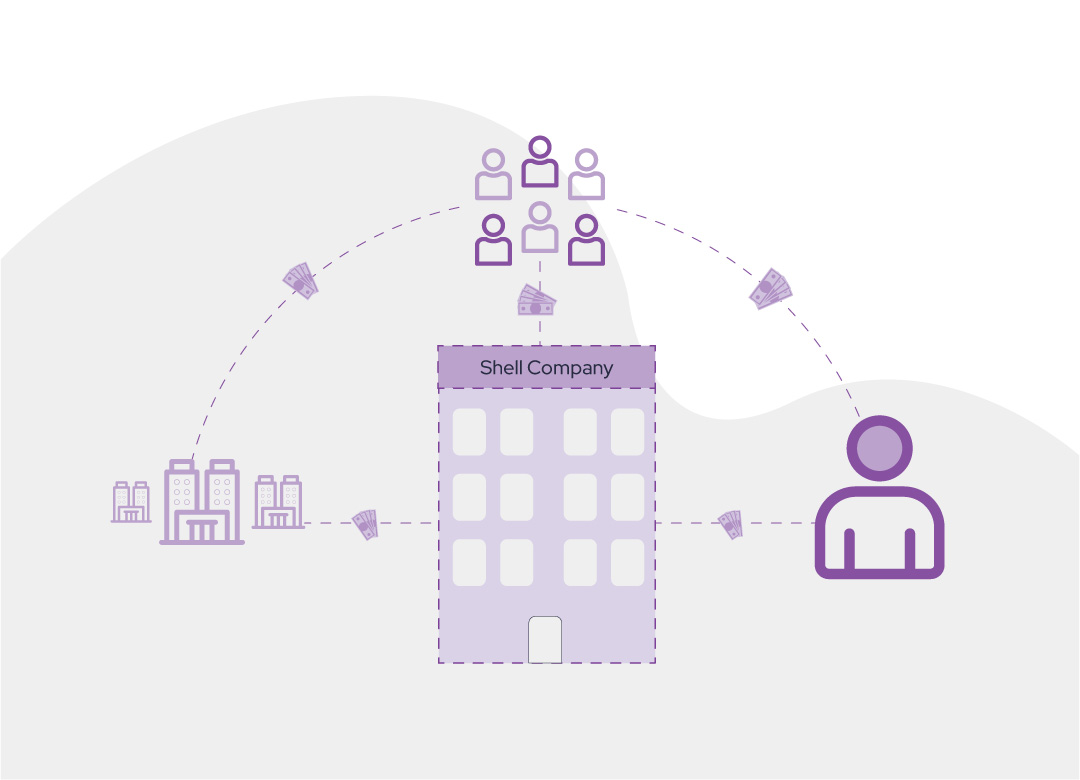

A Shell Company’s corporate structure is not very different from a usual company’s corporate structure. What differentiates the structure of shell companies from usual companies with legitimate and real business operations, assets, and liabilities is the extensive use of nominees to mask the identities of UBOs. Also, the structure of shell companies is often characterised by offshore bank accounts, payable through accounts, complex ownership structures with inter-se ownerships between holdings and several subsidiaries to confuse the scrutinisers.

Don’t Become Collateral in Someone Else’s Shell Game

Avoid Becoming Unknowingly Connected to Shell Companies Used for Illicit Transactions.

How Shell Companies Operate

Shell Companies have no business operations. However, their formation and use are done by following steps:

Quick and easy formation in secrecy jurisdictions

Many tax and compliance neutral or tax haven jurisdictions or jurisdictions that foster secrecy offer quick and easy company formation channels to legitimate investors and criminals alike. These jurisdictions are often preferred by financial criminals due to the secrecy element that facilitates disguising beneficial ownership.

Bank account opening for financial transactions

Once the shell entity is formed, it must have a bank account to resemble a real company that conducts transactions. This bank account of the shell company is then either used or misused by its user for legitimate or illegitimate uses of shell companies discussed earlier.

Complex ownership structure

Once the shell company and its bank account are formed, its beneficial owner usually creates holdings, subsidiaries, and sister concerns to create a complex ownership structure that they may use for conducting illegal activities.

Regulatory Framework for Shell Companies

The Regulatory Framework for shell companies differs from country to country. Some countries strictly prohibit the formation of shell companies, while others only prohibit their misuse for illicit purposes such as tax evasion, ML, FT, PF, sanctions evasion, fraud, etc., while permitting the formation and use of shell companies for legitimate uses such as IP protection.

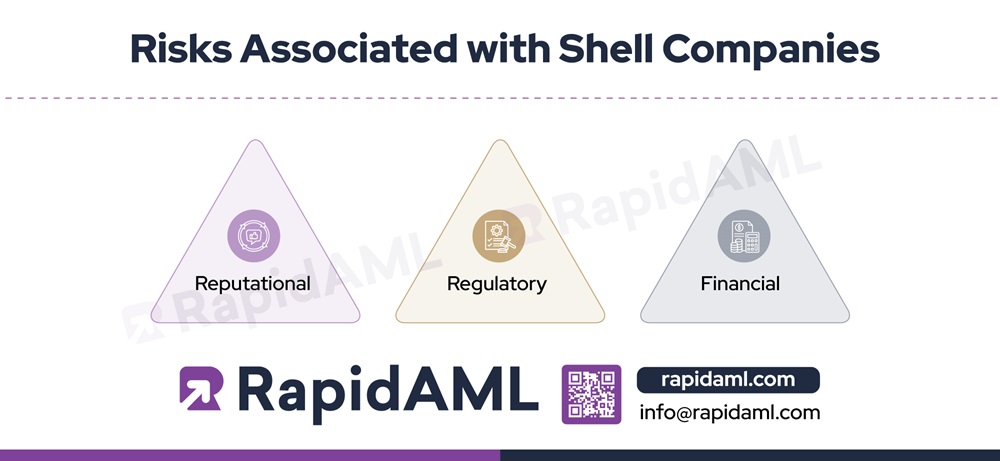

Risks Associated with Shell Companies

Regulated Entities such as Designated Non-Financial Businesses and Professions (DNFBPs), Virtual Assets Service Providers (VASPs), and Financial Institutions (FIs) must exercise caution while conducting business with Shell Companies as it come with its own set of risk factors, such as:

- Reputational: The reputation of the Regulated Entity might get adversely impacted if it is found that the shell entity, with whom they are having a business relationship is, in fact, used for illicit purposes such as ML, FT, PF, or tax evasion, fraud, and any other criminal activities.

- Regulatory: The Regulated Entity having a business relationship with a shell company might end up violating regulatory compliances and requirements by becoming unwitting participants by association with shell companies engaged in illegal activities.

- Financial: The resultant fines and penalties, loss of reputation, or fraud arising from establishing business relationships with shell companies may lead to financial loss risk for regulated entities.

Detecting and Investigating Shell Companies

The identification and investigation of Shell Companies must be integral to every regulated entity’s compliance framework. For instance, every regulated entity’s AML, CFT, and CPF Compliance policies, procedures, systems, and controls should include the steps, tools, workflow, personnel responsibilities, escalation, and alert mechanisms to identify and investigate the element of shell companies while establishing and continuing business relationships with shell companies. All the relevant personnel of the AML Compliance team, such as KYC Analysts, Screening Analysts, Risk Analysts, Transaction Monitoring Analysts, AML Compliance Officer (AML CO) must take active measures to identify the UBOs behind the shell companies and report them if found involved in ML, FT, PF or any other predicate offences to the relevant regulator. The AML Compliance Officer and Senior Management must take the call on whether or not to establish business relationships with shell companies posing high ML, FT, and PF risk to the business and record their decision-making and supporting documentation for the same.

Whether or Not to Conclude Business with Shell Companies: Final Thoughts

Regulated Entities such as DNFBPs, VASPs, and FIs need to be mindful of the legalities and true nature of corporate entity customers, which might be shell companies. In order to successfully identify and mitigate the ML, FT, and PF risks arising out of establishing business relationships with shell companies, RE’s senior management, and relevant client-facing and compliance employees should strive to understand what shell companies are and their modus operandi and leverage AML Software and solutions to enhance detection, monitoring, and risk assessment processes.

Clean On Paper, Risky in Real

RapidAML Helps in Spotting Legal Entities Without Operations That May Be Used for Money Laundering