The UAE real estate market, driven by high-value and cross-border transactions, presents elevated money laundering risks due to complex ownership structures. DNFBPs, such as real estate agents and brokers, and other professionals (for instance, lawyers, notaries, other legal professionals and independent accountants and auditors) involved in real estate transactions must embed UAE-specific name screening to ensure comprehensive regulatory alignment.

Manual sanctions, Politically Exposed Person (PEP), and adverse media screening processes hinder effectiveness, prompting increased adoption of name screening software that automates screening across 700+ global watchlists, while ensuring UAE-specific sanctions screening requirements that prescribe screening across the UAE local terrorist lists, UNSC consolidated lists for robust Targeted Financial Sanctions (TFS) Compliance.

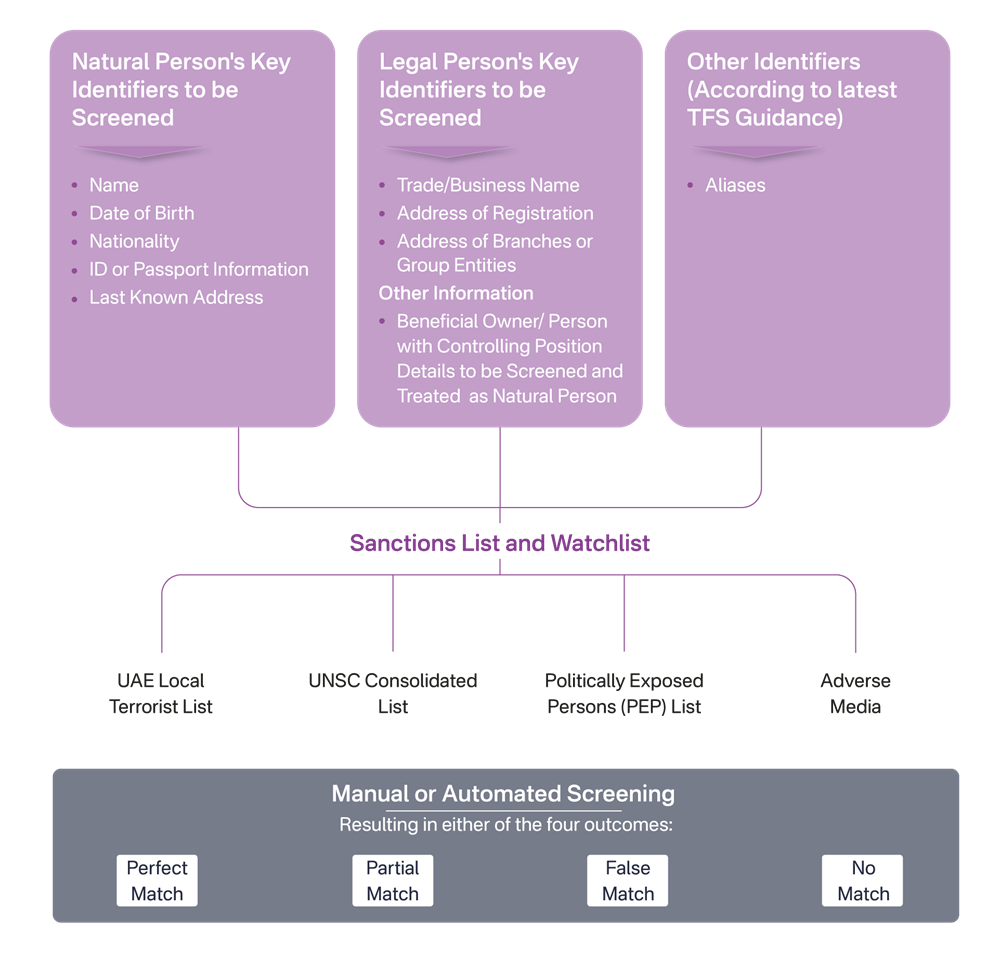

Name screening is the process that involves screening the names and key details of potential, existing clients, and former customers (for a duration of five years after cessation or termination of business relationship) to identify whether individuals or corporates customer’s names appear while screening against UAE local list or UNSC consolidated lists, also commonly referred to as the sanctions lists, as required under the UAE’s laws on Anti-Money Laundering (AML), Combating Financing of Terrorism (CFT), Targeted Financial Sanctions, and relevant UN Security Council Resolutions (UNSCRs).

When should Real Estate Brokers and Agents perform Name Screening as per UAE AML regulations?

Real estate agents and brokers should ensure that they have a process for screening customers and prospective customers against Sanction Lists, and perform background checks to identify any potentially adverse information, particularly their association with financial crimes or their status as local or domestic and current or former PEP.

Name Screening needs to be carried out by Real Estate Brokers and Agents in UAE at the following key stages:

RapidAML Detects the Risk before They Reach You

Stay Compliant and Ahead with Instant Alerts

Name Screening for real estate agents, real estate brokers, or professionals involved in real estate transactions can be broadly classified into three categories: sanctions screening, PEP screening, and adverse media screening. Let’s dive into each type for greater clarity.

Refer to our YouTube Video: Introduction to Name Screening: The UAE Standpoint | RapidAML

Purpose: Sanctions Screening serves the following purposes:

Real estate entities in the UAE must establish a comprehensive Customer Due Diligence (CDD) framework to identify clients, their business activities, and the nature of property-related dealings. This includes verifying customer identities, vendors, and ultimate beneficial owners (UBOs) using reliable independent sources. Name screening is a critical component of CDD, enabling firms to check whether individuals, UBOs (for legal entities), or senior management appear on sanctioned lists such as the UN Consolidated List, UAE Local Terrorist List, or other international sanctions registers.

TFS Compliance: Under Cabinet Decision No. 74 of 2020, Targeted Financial Sanctions (TFS) compliance is mandatory. Real estate businesses must register with the UAE Executive Office for Control and Non-Proliferation (EOCN) and conduct ongoing screening of clients, suppliers, and business partners to ensure no association with designated persons or entities.

For more insights into Sanctions and TFS Compliance Requirements in UAE, refer to Sanctions Compliance Best Practices for DNFBPs and VASPs.

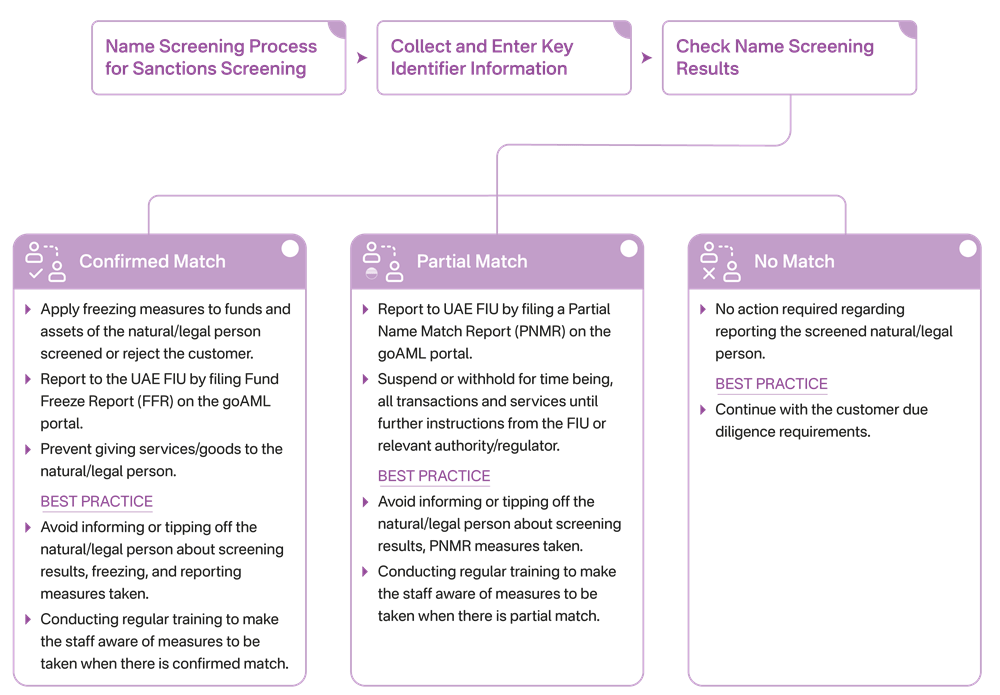

Process: The process for sanctions screening for Real Estate Brokers and Agents is illustrated here for a better understanding.

Refer to our YouTube Video: The orderly process of customer screening to ensure AML compliance | RapidAML

Purpose

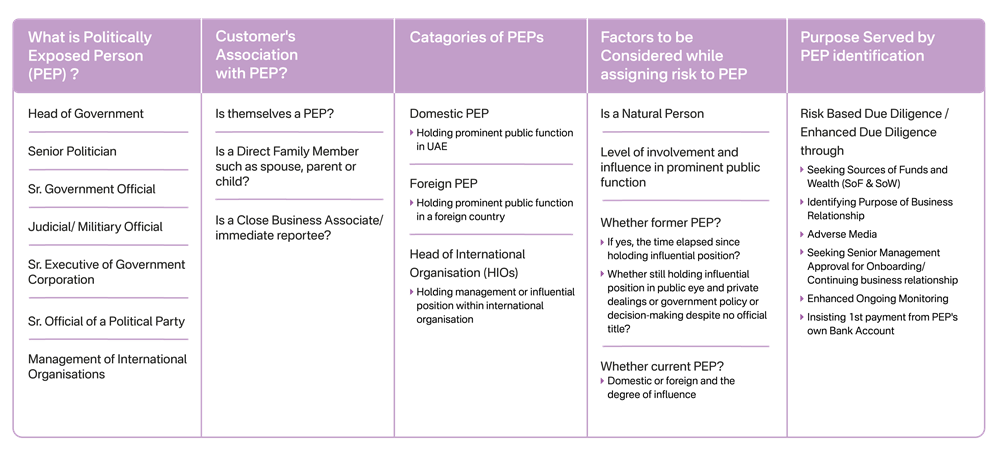

Real estate businesses in the UAE, as DNFBPs under the AML/CFT framework, must identify Politically Exposed Persons (PEPs) and screen customers, vendors, and business relationships to determine whether any individual, such as the customer, UBO, person in control, or authorized signatory of a legal entity, is a domestic or foreign PEP or closely associated through familial or business ties. PEP screening is especially critical when dealing with foreign clients, given the heightened risk of corruption or money laundering.

Enhanced Due Diligence (EDD) may be triggered where PEP risks are present. Due to the complexity of PEP customer profiles and the cash-intensive nature of property transactions, firms may encounter false positives or negatives during manual screening. Implementing AML software with automated name screening capabilities helps mitigate these issues, improving detection of links to financial crimes like fraud, bribery, or predicate offences.

Based on identification, transaction history, and screening outcomes, real estate entities must carry out customer risk profiling—classifying clients into high, medium, or low ML/FT risk tiers under Customer Risk Assessment (CRA) protocols.

Process: For better understanding, the process for PEP screening for Real Estate Brokers and Agents in the UAE is illustrated here.

Purpose

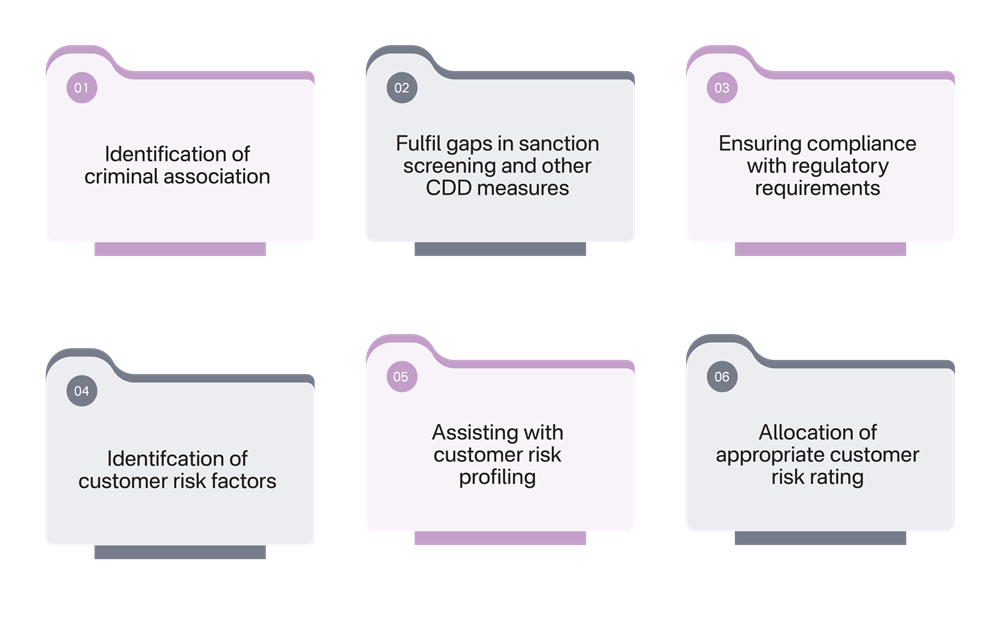

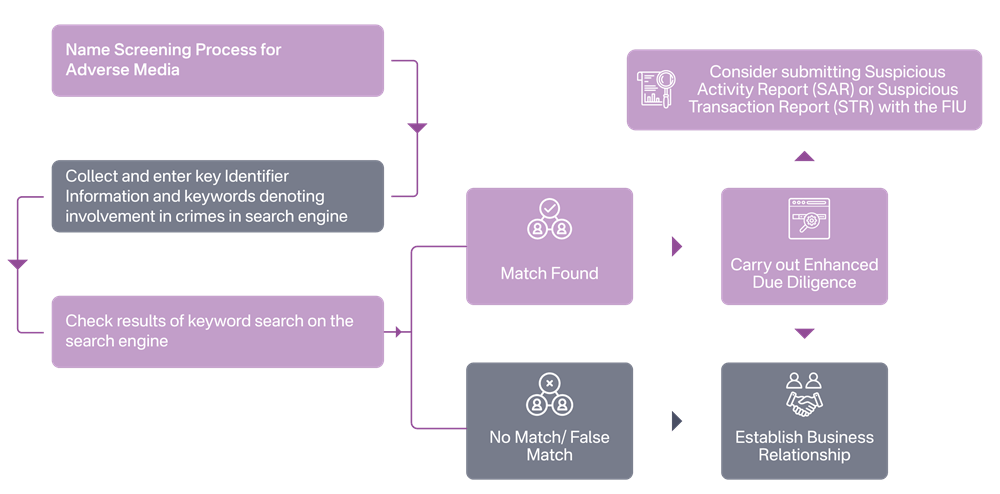

The purpose of adverse media screening for real estate professionals involves scanning publicly available digital sources for negative news involving prospective or existing clients, or associates, such as allegations of bribery, fraud, corruption, trafficking, or other predicate crimes. Any indication of reputational risk must prompt further investigation and risk rating adjustments.

This process complements sanctions screening and forms a part of Customer Due Diligence by helping real estate firms uncover blind spots that sanctions and PEP checks might miss. Adverse media insights support Customer Risk Assessments (CRA) and guide decisions on applying Enhanced Due Diligence (EDD) measures for high-risk profiles in property transactions.

Process: The process of Adverse Media is illustrated below:

For more insights into Adverse Media, refer to Integrating Adverse Media Screening into AML Framework: A Guide for DNFBPs and VASPs

Refer to our YouTube Videos:

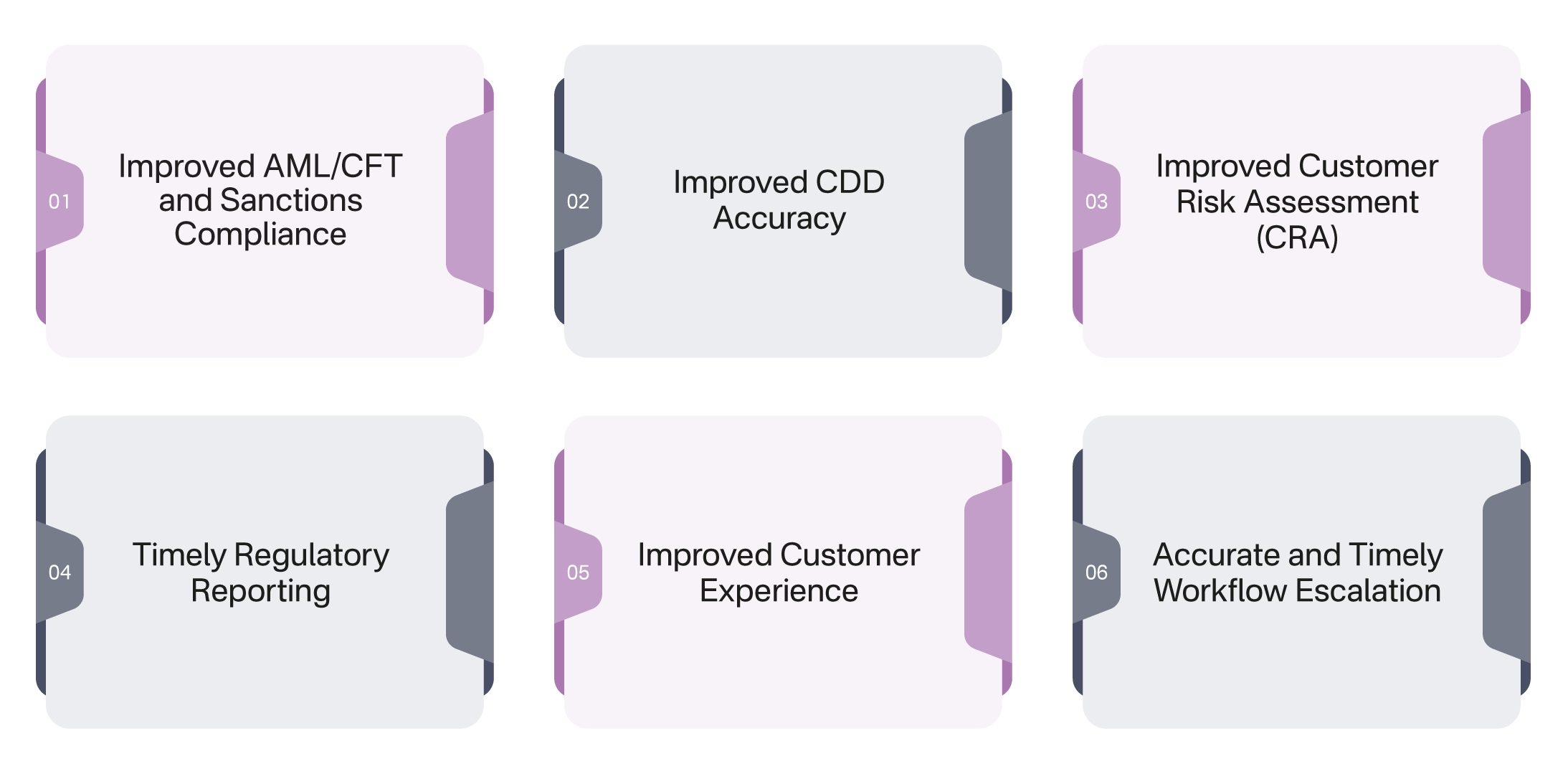

In UAE real estate sector, name screening is essential for AML/CFT and Targeted Financial Sanctions (TFS) compliance. Real estate brokers, developers, and agents must employ robust name screening tools. Effective Name Screening is a non-negotiable AML/CFT and TFS Compliance requirement due to the following factors:

1. Improved AML/CFT and Sanctions Compliance

Ensuring a stringent AML/CFT and TFS or Sanctions Compliance Policy, Procedures, and Controls in place helps real estate agents, brokers, and professionals involved in real estate transactions to ensure that their TFS, i.e., sanctions compliance, is made leakproof through the use of a well-calibrated Name Screening tool. This ensures that there is no scope for sanctioned individuals or entities to escape precise scrutiny through proper use of reliable screening solutions.

How AML/CFT and TFS or Sanctions Compliance Policies, Procedures, and Controls Help Real Estate Brokers and Agents with Effective Screening.

2. Improved CDD Accuracy

In UAE’s real estate sector, name screening helps the Customer Due Diligence (CDD) process by detecting risks tied to individuals or entities involved in property transactions. When aligned with business-specific risk factors and supported by accurate results, name screening significantly enhances the integrity of CDD.

The five core components of CDD include:

1. Know Your Customer

2. Name Screening

3. Customer Risk Assessment (CRA)

4. Enhanced Due Diligence (EDD)

5. Ongoing Monitoring

Among these, name screening poses the highest vulnerability due to challenges such as:

Errors in this phase may skew risk ratings, misguide periodic reviews, and distort the overall assessment of customer risk, impacting critical decisions in the CRA and EDD phases. UAE real estate firms must adopt well-calibrated, regularly tested name screening tools that ensure accurate identification, reduce reliance on manual analysis, and reinforce a reliable, compliant AML/CFT framework.

3. Improved Customer Risk Assessment (CRA)

Customer Risk Assessment is an integral part of the CDD process that follows Name Screening. Real estate agents and brokers in the UAE must recognise that money laundering and terrorism financing (ML/FT) risks vary significantly across customer segments. For example, middle-income UAE nationals engaged in property transactions for personal use may present lower ML/FT risks compared to foreign corporate clients with complex ownership structures transacting for resale or investment purposes. AML/CFT resources and due diligence measures must therefore be proportionately allocated based on assessed risk profiles.

4. Timely Regulatory Reporting Obligation of Real Estate Brokers and Agents

In order to ensure compliance with the TFS obligations, Real Estate Brokers and Agents must implement the following four steps:

Regulatory Reporting Obligations for Real Estate Brokers and Agents in UAE

Real estate is also required to design and implement adequate mechanisms to identify potential ML/FT risk indicators and report suspicious activities or transactions to the FIU through goAML portal in a timely manner if any suspicious behavior is observed in a customer prior to a transaction (SAR) or after a transaction (STR).

However, real estate professionals must bear in mind that if any of their customer’s names appear on watchlists other than UN Consolidated List and UAE local terrorist list, such as OFAC, HMT, INTERPOL, and the likes, then they are not supposed to file CNMR/PNMR, instead they must file SAR/STR, depending on stage of business relationship to notify UAE FIU of such a screening match (partial or complete).

Ultimately, the accuracy, timeliness and quality of Regulatory Reports are directly dependent on the efficacy of outcomes generated by performing name screening.

5. Improved Customer Experience

In the UAE real estate sector, a smooth and user-friendly customer onboarding process hinges on the efficient collection of client details through KYC methods such as self-KYC or eKYC. By integrating name screening tools with KYC platforms, real estate firms can facilitate the easy upload and verification of customer information. This not only enhances the onboarding experience but also strengthens AML defences by proactively identifying and mitigating potential risks, helping real estate agents, brokers, and developers safeguard their operations against exploitation by financial criminals.

6. Accurate and Timely Workflow Escalation

In UAE real estate sector, efficient name screening enables rapid disambiguation of customer matches, allowing Screening Analysts to promptly escalate cases to the relevant KYC Analyst, AML Risk Analyst, or Compliance Officer when necessary. A well-functioning screening system significantly streamlines the AML compliance process, enhancing both speed and accuracy.

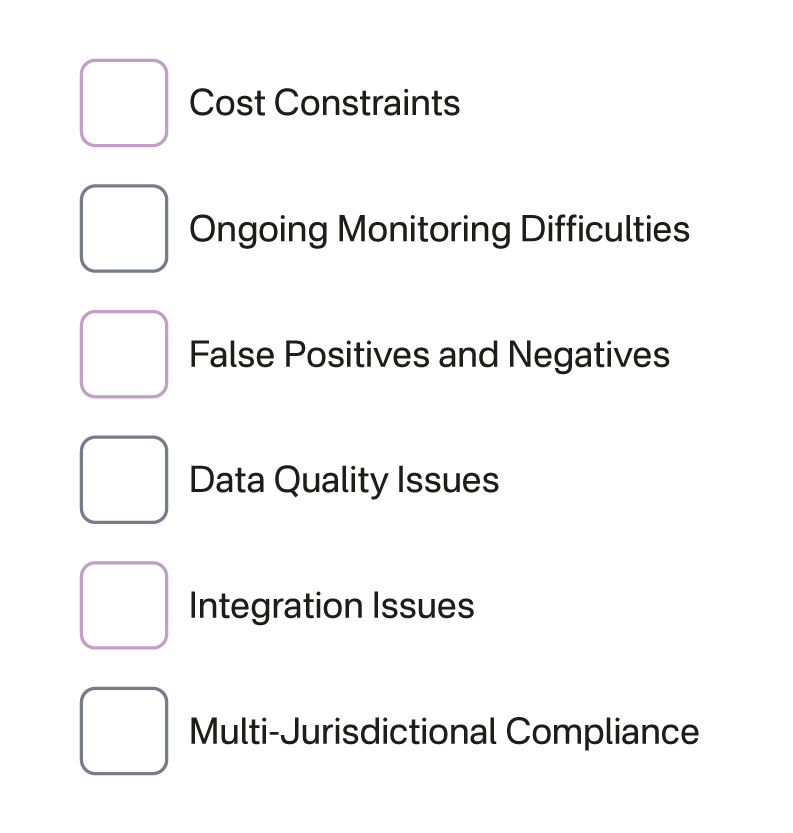

Name Screening is seen as a hurdle while implementing these procedures. Some common pain points are as follows:

1. Cost Constraints

Conducting Screening, either manually or through automation, necessitates both trained personnel and effective screening software. For many Real Estate Brokers and Agents, especially smaller firms, this process can be resource-heavy and financially straining, affecting their profit margins. It becomes essential for them to adopt name screening software that is both technologically advanced and cost-efficient, helping to strike a balance between meeting compliance requirements and avoiding the high costs of non-compliance.

2. Ongoing Monitoring Difficulties

Name screening is not a one-time procedure limited to the initial stages of a client relationship. Real estate brokers and agents are expected to continuously monitor and update the screening status of their existing clients for the entire duration of the business relationship, up to five years after the business relationship has ended and even during weekends and public holidays. They must also adhere to their obligations under the Targeted Financial Sanctions (TFS), which mandate screening of current and former clients against updated versions of the UAE Local Terrorist List and United Nations Sanctions List.

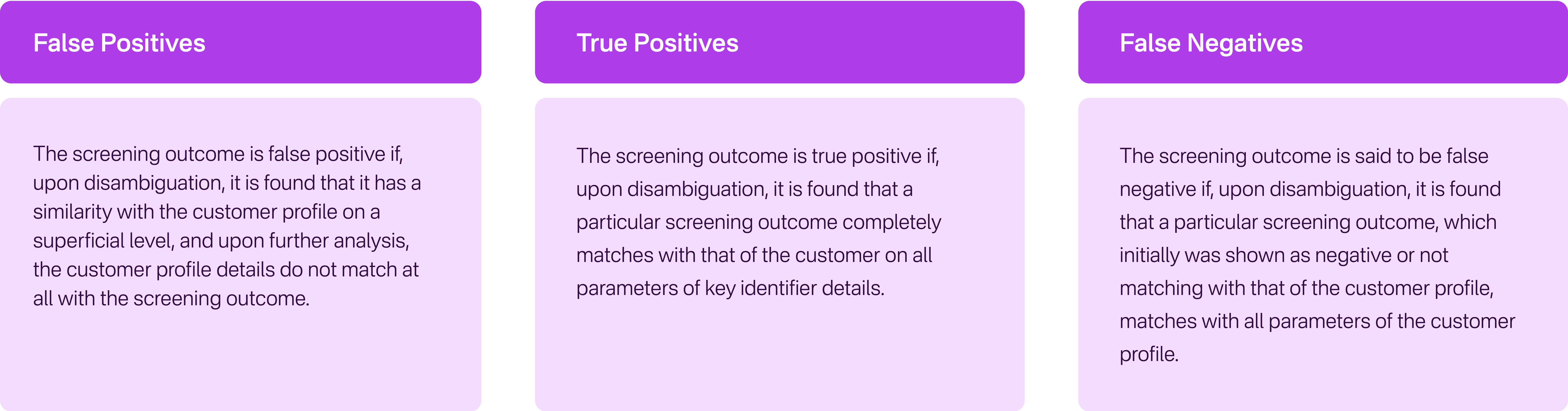

3. False Positives and Negatives

False positives occur when screening software produces potential matches based on partial similarities with client data. However, further investigation reveals that the client does not actually correspond to any listed or individual entity.

False negatives, however, are the opposite – they arise when the system fails to flag a client who should have been matched.

Reasons for False Positives in Name Screening by Real Estate Brokers and Agents

False positives can significantly reduce the efficiency of name screening, requiring brokers and agents to spend excessive time on verifying irrelevant matches. This often happens when the screening system is not finally calibrated.

4. Data Quality Issues

The accuracy and format of client data collected by real estate brokers and agents play a crucial role in the effectiveness of name screening. If this data is incorrect, outdated, incomplete, or stored in inconsistent formats, it directly hampers the reliability of the screening process. Name screening tools rely on clean and structured data for accurate results, and any compromise in data quality undermines the entire process.

5. Integration Issues

Real Estate Brokers and Agents also face challenges when attempting to integrate various tools, such as AML/CFT compliance software, client onboarding processes, customer relationship management tools (CRM), and regulatory reporting platforms. These integration difficulties can stem from technical incompatibilities, outdated systems, licensing limitations, or insufficient scalability, all of which hinder seamless operations and regulatory compliance.

6. Multi-Jurisdictional Compliance

Real Estate Brokers and Agents operating across different jurisdictions or serving international clients find it challenging to ensure compliance with various AML/CFT laws. They must consider multiple international and domestic sanction lists and stay aligned with both local and global TFS obligations. Navigating this multi-layered compliance environment demands a strategic approach.

Are Operational Hurdles Slowing Your Deals?

Learn How to Make Name Screening Quick, Clean, and Compliant

Recognising the problems or difficulties in screening is just the first step for real estate brokers and agents. It helps them become aware that a problem exists. The next important step is to understand what effects or consequences these problems can have. Knowing these consequences helps real estate agents see how technical the issues are and how they can affect their daily lives.

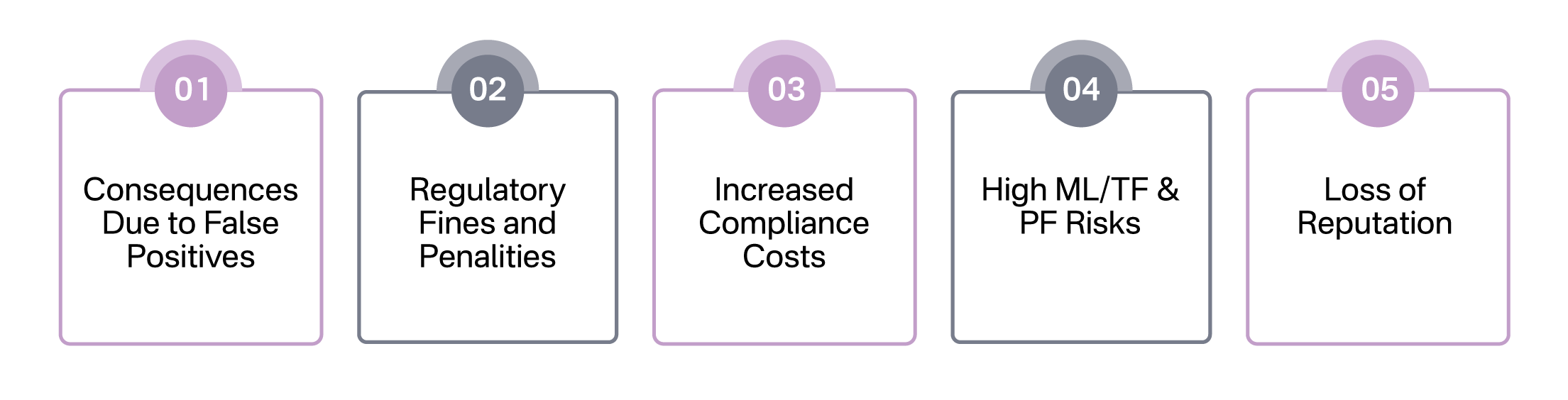

Consequences Due to False Positives

The challenge of false positives brings along a series of associated consequences. Real Estate Brokers and Agents experiencing a high volume of false positives must also manage the following issues.

Consequences of High False Positive Rates on Real Estate Brokers and Agents during Sanctions Screening Outcome Analysis

Increased Workload:

The Screening Analyst and the AML Compliance officer or Money Laundering Reporting Officer (MLROs) often end up with a heavier workload because they have to sort through many false positive matches. These unnecessary matches take up valuable time and energy without adding any actual value to the business.

Delays in Customer Onboarding:

When Screening Analysts spend too much time dealing with false positives, it slows down the entire customer onboarding process. This delay can frustrate customers, create a bad onboarding experience and increase the chances of potential clients dropping out.

Delays in Concluding Business Transactions:

If the onboarding process is delayed, naturally so are the business deals. This leads to slower turnaround times (TAT), which can reduce the overall efficiency and profitability of real estate brokers and agents.

Inefficient Screening Process:

A high number of false positives is a clear sign that the screening process is inefficient. Instead of helping the compliance staff work faster and more accurately, the system creates more confusion and stress, indicating that the screening tool or process needs serious improvement.

Fines and Penalties

Too many false positives might also mean that the screening system is not reliable. It could fail to identify real threats or sanctioned individuals. If real estate brokers and agents don’t spot and report these high-risk clients correctly, they may violate AML (Anti-Money Laundering), TFS (Targeted Financial Sanctions), or PEP (Politically Exposed Persons) compliance rules, resulting in fines and legal consequences.

Reputational Damage:

When a real estate broker or agent is penalised for non-compliance, the damage goes beyond financial loss. Their reputation suffers, and their credibility is questioned. This loss of trust can affect long-term business relationships and client confidence.

Obstruction of Actual Threats:

Having too many false positives can also mean missing out on spotting real threats. Criminals might slip through and use real estate services to carry out illegal activities. This increases the risk of real estate brokers and agents unknowingly being involved in money laundering, terrorist financing, or proliferation financing.

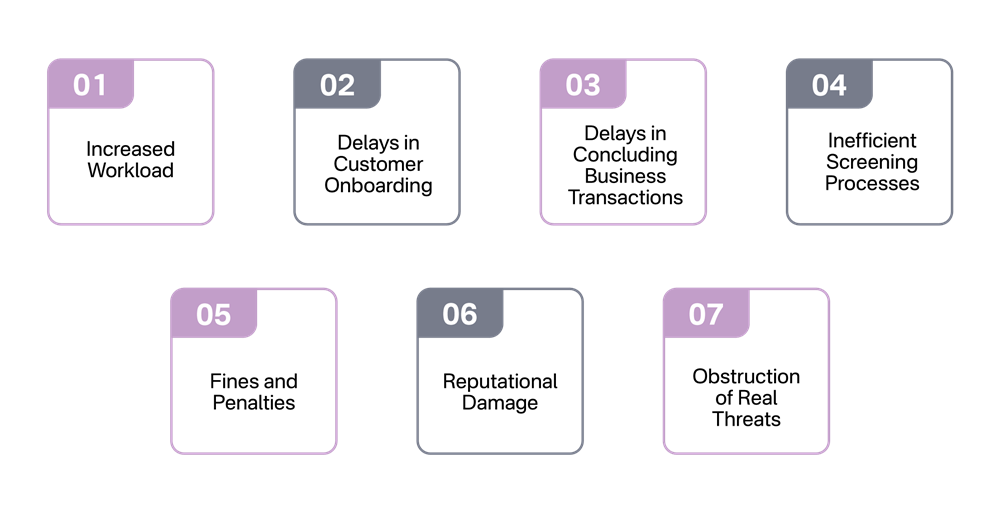

Regulatory Fines and Penalties

For real estate brokers and agents operating across different countries, the challenges of ongoing monitoring, poor data quality, or delays in screening can lead to violations of local or international laws. This can result in heavy fines and penalties for failing to meet AML/CFT requirements in one or more jurisdictions.

Loss of Business Reputation

Real estate brokers and agents struggling with cost issues, monitoring challenges, and poor data quality are at a high risk of damaging their business reputation. Even one fine, penalty, or negative news report can seriously harm how clients and partners view them, especially if the news involves unintentionally facilitating financial crimes.

High ML/TF & PF Risks

It is understood that weak or inefficient name screening leads to higher risks of money laundering (ML), terrorist financing (TF), and proliferation financing (PF). These risks can be greater than was predicted in the company’s process of Enterprise-Wide Risk Assessment (EWRA).

Increased Compliance Costs

Dealing with false positives, system integration issues, and meeting the requirements of multiple jurisdictions raises the cost of compliance. Hiring experienced AML professionals and implementing strong systems to cover all jurisdictions is expensive. Integration problems also create inefficiencies.

Screening Errors Should Not Cost Your Business

Learn How RapidAML Takes the Pain Out of Compliance

Once Real Estate Brokers and Agents understand the serious risks of poor name screening, they can better protect themselves by using RapidAML, which helps solve common screening issues.

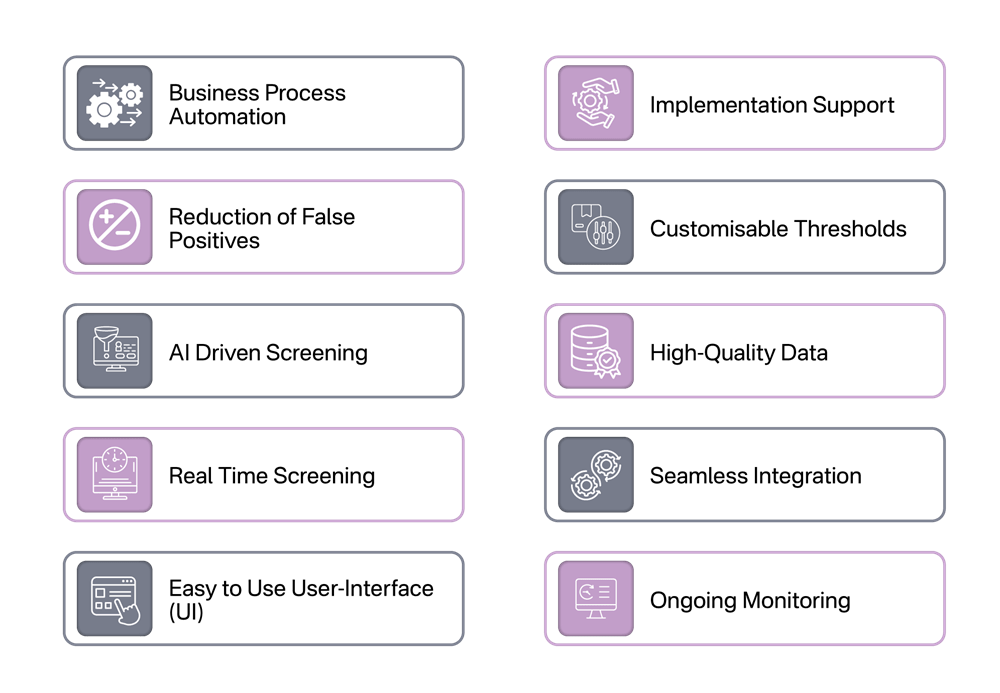

RapidAML simplifies Name Screening Obligations for Real Estate Brokers and Agents in UAE through its multi-faceted capabilities, such as the following:

Business Process Automation

Business Process Automation means using technology to handle repetitive tasks that are usually done by hand. This is useful for name screening, where one customer is screened after another in the same way. RapidAML’s Screening Software helps real estate brokers and agents automate this process, making it faster and easier.

Reduction in False Positives

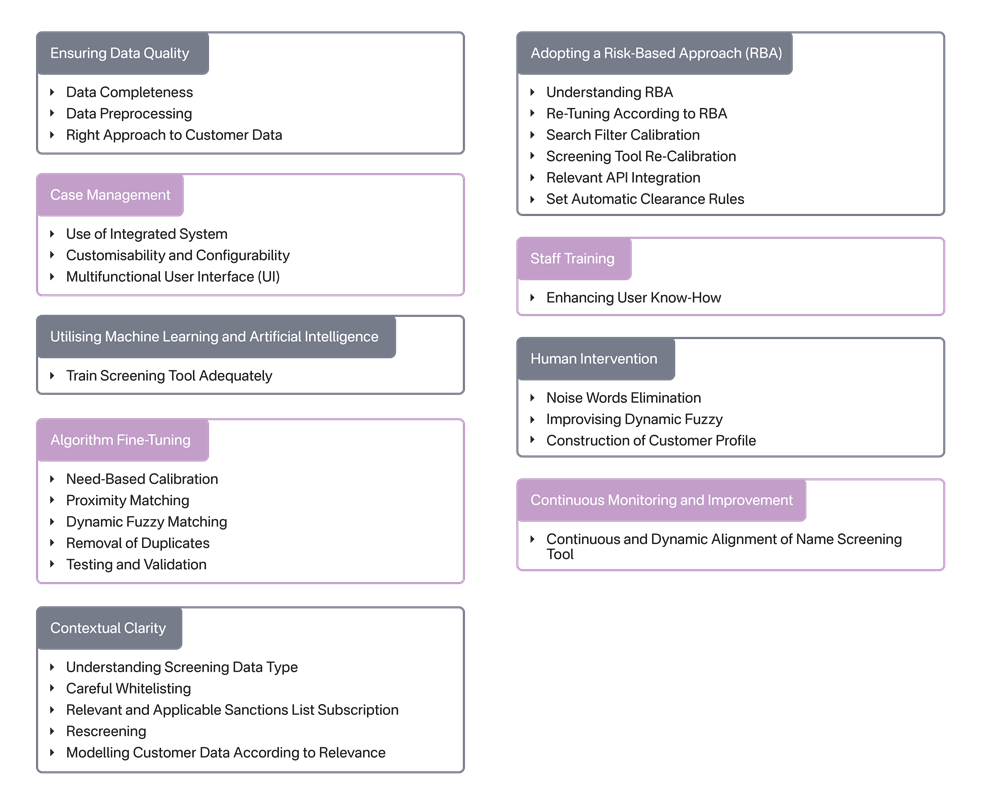

False positives are a major problem for real estate brokers and agents in the UAE. RapidAML helps reduce these by using fuzzy logic, which considers language and pronunciation differences. Also, the software can be customised and adjusted to suit different needs, which lowers the chances of getting false matches.

How RapidAML Helps Real Estate Brokers and Agents Minimise False Positives

Refer to our YouTube Video: Effective Approaches to Reducing False Positives in Sanctions Screening | RapidAML

AI-Driven Screening

RapidAML uses AI and fuzzy matching to reduce the time spent sorting through false positives. This makes it easier and faster for analysts to make decisions. RapidAML helps cut down the time taken while disambiguating a high number of false positives and simplifies customer onboarding.

Real-Time Screening

In name screening, speed matters. If watchlists or sanction lists are outdated, the results won’t be reliable. Also, slow screening can cause missed matches. RapidAML fixes this by providing real-time screening using the latest data and completing the screening very quickly.

Batch Screening

Automating one task at a time isn’t enough. RapidAML allows bulk screening, so that many customers can be screened at once. Then, the screening analyst can review and disambiguate each result individually, balancing speed with TFS compliance. This makes the screening process quick and reliable.

Easy-to-Use User Interface (UI)

RapidAML has a simple and user-friendly UI that makes it easy for the compliance team to use. Screening software users such as screening analyst need not be tech-savvy to understand and use it. RapidAML reduces the learning curve for first time screening software users in the real estate sector.

Easy Disambiguation

RapidAML makes it easy to disambiguate and tell whether a match is confirmed, partial, or a false match by organising screening results into categories like Sanctions, PEPs, and Adverse Media outcomes. This helps screening analysts to quickly understand what kind of match it is, i.e., false, partial, or full.

Document Repository

RapidAML lets users store records and documents related to sanctions screening for as long as required by the regulatory authority. This cloud-based storage system helps real estate brokers and agents meet record-keeping requirements with ease, keeping the audit and inspection ready.

Kanban Board for Task Management

Screening involves many people: the front office collects documents, screening analysts do the screening, and the compliance officer makes the final call. The KANBAN Board shows who is working on what and how far they are. This keeps the whole team aligned and organised.

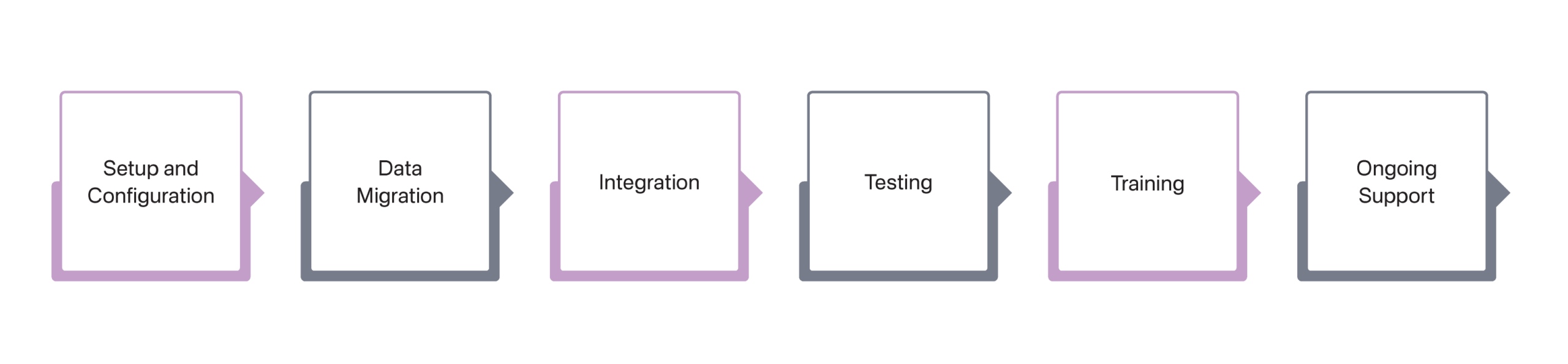

Implementation Support

RapidAML doesn’t just provide the software and leave real estate brokers and agents on their own. It offers training and support, so users know how to screen, generate reports, manage cases, and adjust the system as needed. This includes multiple aspects such as:

RapidAML Screening Software Implementation Process for Real Estate Brokers and Agents in UAE

Customisable Thresholds

Every real estate firm has different AML, CFT, and TFS compliance needs. RapidAML allows customisation of thresholds, screening duration and watchlist criteria so that screening results match what each firm is looking for. This improves accuracy and relevance.

High-Quality Data

RapidAML produces accurate and detailed data about screenings, reports, and case files. This not only helps with record-keeping but also supports the compliance officer in making informed decisions without human error. All data is linked back to the document repository for quick access.

Seamless Integration

Integration means different software systems working well together. RapidAML integrates smoothly with other tools used by real estate firms, like onboarding systems, CRM, billing tools, and more, so that information flows easily between them. This improves efficiency.

Ongoing Monitoring

AML compliance is not a one-time task. Real estate brokers and agents need to keep an eye on customer profiles throughout the relationship and even after the business relationship has ended. RapidAML allows the compliance officer to label customer profiles (e.g., active, dormant, or exit) and then keeps monitoring them.

Stop Struggling with False Positives

Let RapidAML Smooth the Cracks in Your Compliance Foundation

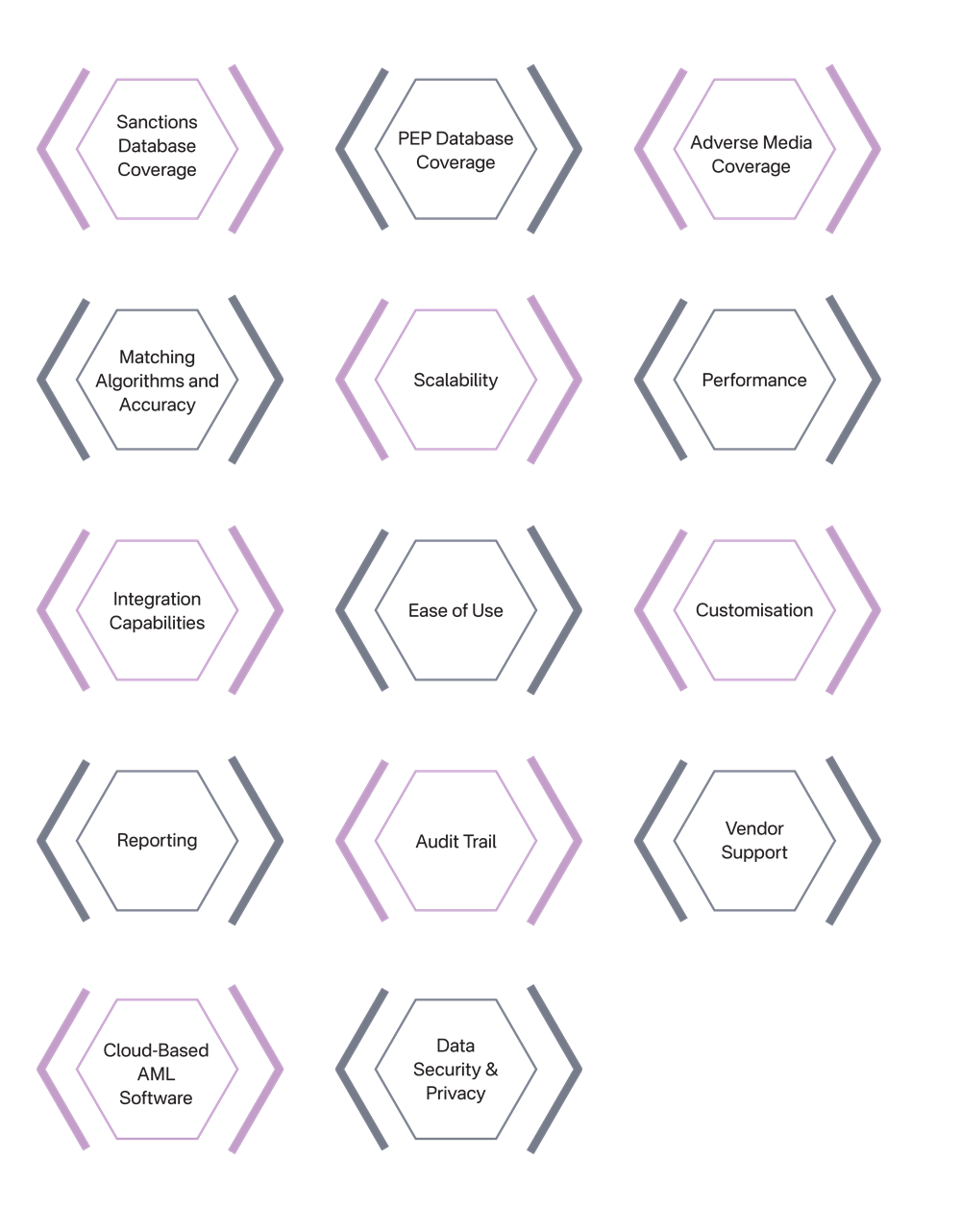

Rapid AML Screening Software is specially designed to meet the UAE’s AML/CFT and Targeted Financial Sanctions (TFS) requirements for Real Estate Brokers and Agents. It also helps solve the common problems Real Estate Brokers and Agents usually face during screening. The key features of RapidAML, explained below, show why it is the ideal solution for Real Estate Brokers and Agents in UAE looking to improve their screening process.

Features Matter as Much as Location

See What Makes RapidAML the Prime Property of Compliance Solutions

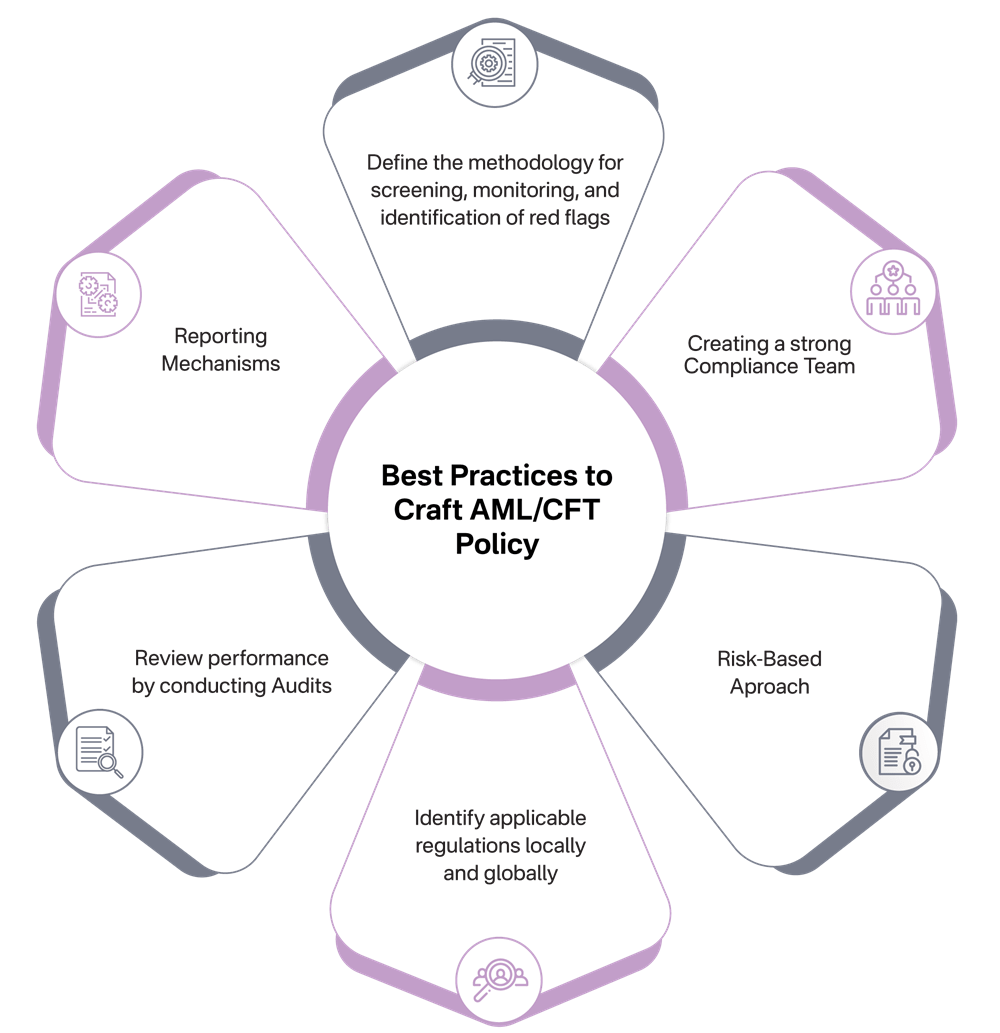

Success stories are the result of strategic planning, continuous improvements, and consistent effort to align the real estate sector with regulatory compliance requirements. Here are some best practices to achieve the successful implementation of screening software:

Refer to our YouTube Video: Best Practices in Sanction Screening Software Implementation | RapidAML

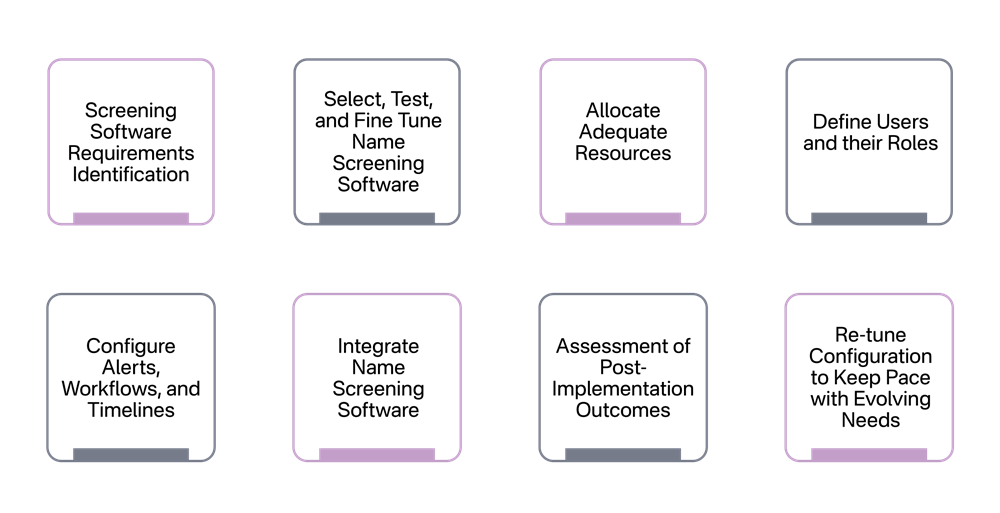

Screening Software Requirements Identification

A real estate professional in UAE must have clarity on their screening obligations based on their unique needs, which depend on risk factors such as markets, operating geographies, delivery methods, and transaction modes and volumes. Simply put, the screening solution selected must align with the latest EWRA of the real estate and TFS obligations while supporting their long-term vision and growth strategy. This ensures that they are screening prospects and clients against relevant jurisdiction-based watchlists and sanctions databases.

Identify Migration Requirements

Whether migrating from manual processes to RapidAML, from another screening solution to RapidAML, or switching between name screening tools, Real Estate Professionals must first understand the technical and operational requirements of the new solution. Identifying these migration prerequisites is critical for formatting and structuring existing customer data in a way that the new tool can accurately process. If data alignment is mishandled, it could result in data loss, recordkeeping violations, business disruptions, reputational damage or even breaches of data protection laws.

Select, Test, and Fine-Tune Name Screening Software

Testing the screening software before full implementation is essential. A test run helps Real Estate Professionals identify which areas of the solution require adjustments or customisation to match their operational structure. For example, the screening tool should allow workflows and the escalation process to be tailored according to their internal hierarchy. Real Estate Professionals must also configure parameters such as matching thresholds, whitelisting criteria, and activity-specific filters. These settings should be documented in their AML/CFT policies to reflect the organisation’s adopted control measures.

Allocate Adequate Resources

Name Screening is a regulatory obligation and requires adequate resource allocation. While compliance has its costs, these are preventive in nature, shielding Real Estate Professionals from the far greater expenses of non-compliance, including hefty fines, criminal penalties or license revocation. Real Estate professionals must conduct a cost-benefit analysis and dedicate sufficient funds and staff to ensure long-term use of the screening software. Investing in a reliable solution should be viewed as a necessary safeguard, akin to a vaccine, protecting them from the widespread consequences of regulatory failures.

Define Users and their Roles

It is essential for Real Estate Professionals to create an implementation roadmap where employee responsibilities, approval hierarchies and workflows are closely mapped to the chosen screening solution. This is best achieved by clearly defining users and assigning role-specific permissions within the software. A successful mapping exercise directly impacts the success of the implementation process. Vendor support plays a key role here by helping staff transition from pre-implementation practices to new workflows through training and guidance, ensuring the team is equipped to handle the screening tasks from day one.

Configure Alerts, Workflows, and Timelines

Real Estate Professionals should fully utilise the customisation features of their chosen screening software by configuring alerts, escalation routes, and task timelines. These adjustments enable more effective management of daily operations and ensure timely responses to potential compliance issues. When these configurations are combined with a robust screening tool, they can strengthen their AML/CFT compliance, streamline operations, and reduce delays or missed alerts, significantly enhancing the quality of name screening procedures within the organisation.

Integrate Name Screening Software

Real Estate Professionals must leverage the integration features of their screening software to optimise efficiency. Integration reduces redundancy and cuts down operational expenses by allowing seamless connectivity with CRM, invoicing, accounting systems and other AML tools such as transaction monitoring and customer risk profiling. They should also consider integrating with case management systems to create a unified compliance interface, enabling teams to manage screening, investigations and escalation cases under one comprehensive dashboard with minimal manual input.

Assessment of Post-Implementation Outcomes

After implementation, Real Estate Professionals must regularly evaluate the effectiveness of their screening solution. This includes tracking outcomes to determine whether the tool meets compliance goals, or if issues like high false favourable rates or excessive manual review work persist. Such assessments reveal whether software re-configuration, staff training or a complete software change is needed. This also helps determine if the software is scalable and suitable for future expansion.

Re-tune Configuration to Keep Pace with Evolving Needs

Real Estate Professionals must routinely update and fine-tune their screening software to reflect changes in applicable sanctions regimes, regulatory amendments, and operational expansion. This includes adjusting jurisdictions, revising watchlist subscriptions, or updating ongoing monitoring preferences. These changes must also be documented and reflected in AML/CFT policies. Ensuring procedural updates are in sync with system changes helps maintain compliance, avoids regulatory breaches, and reduces the likelihood of receiving audit findings or heightened regulatory scrutiny due to outdated configurations.

Surprises Belong Only in Property Listing, Not Contracts

Name Screening Done Right Keeps You Compliant and Clients Trustworthy

Name screening for Real Estate Professionals in the UAE can be streamlined through a carefully designed implementation strategy. RapidAML’s solutions, combined with its consulting expertise, support Real Estate Professionals in effectively managing the complexities of AML/CFT and TFS compliance, especially in relation to their screening obligations.

Get Started

Contact Us