In the fight against Money Laundering and Financing of Terrorism (ML/FT) globally, the effectiveness of compliance frameworks often depends on how well the institutions know their customers. Traditional Know Your Customer (KYC) processes have relied on periodic reviews or “re-KYC”, but this approach usually leaves long gaps during which suspicious customers and their activities may go unnoticed.

Perpetual KYC (pKYC) has emerged as a global best practice to close these gaps by enabling continuous monitoring and updating of customer information. Rather than treating Customer Due Diligence (CDD) as a one-time or occasional exercise, pKYC turns it into a dynamic and ongoing process. This shift allows businesses to detect risks more quickly, respond to unusual activities in real time, and maintain compliance in line with rising regulatory expectations.

As money and markets evolve at lightning speed, regulators expect businesses to go beyond ticking boxes when it comes to CDD. The pKYC is increasingly seen as the future of due diligence, helping Financial Institutions and other entities meet global Anti-Money Laundering (AML) standards more effectively.

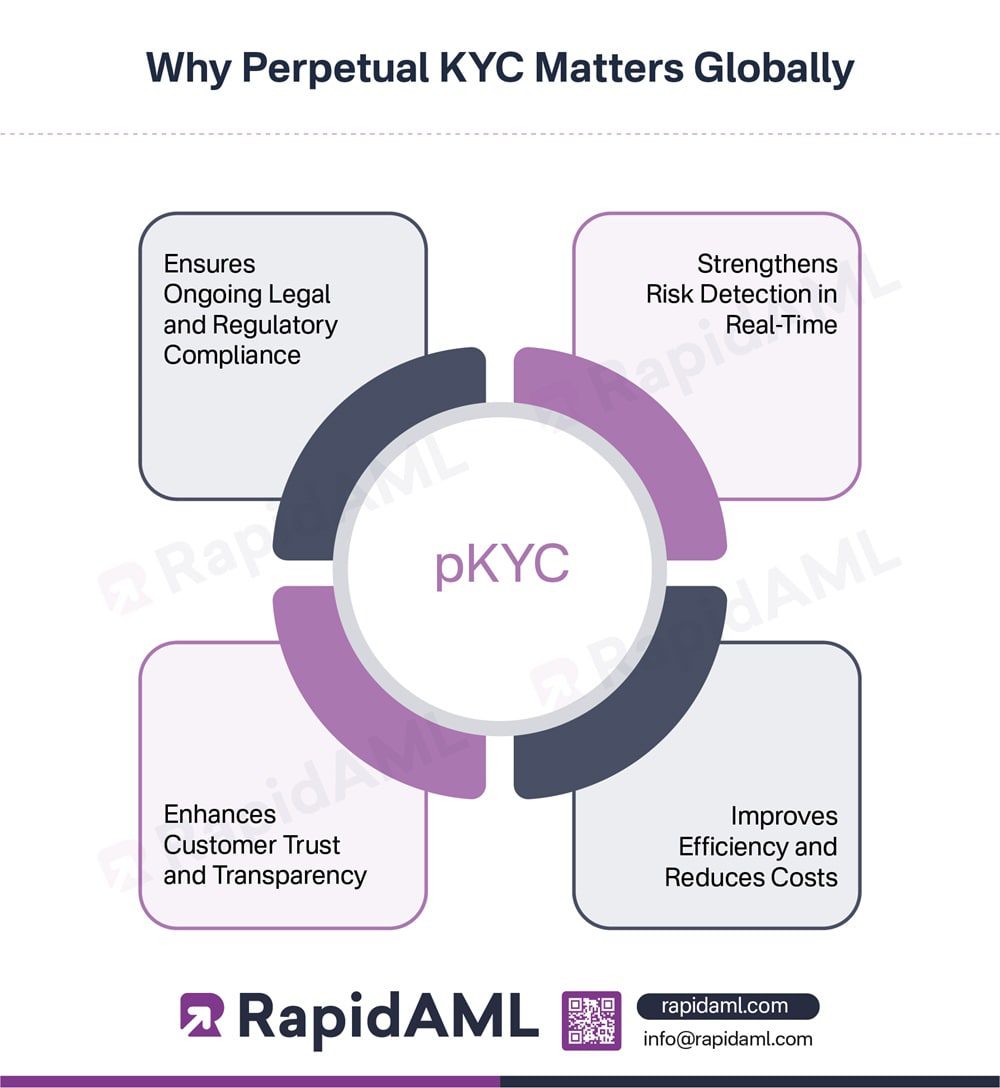

Ensures Ongoing Legal and Regulatory Compliance

Financial Action Task Force (FATF) Recommendation 10 requires firms to maintain accurate and up-to-date customer information, particularly for higher-risk categories of customers. pKYC aligns with this by embedding real-time monitoring into operations, ensuring institutions stay compliant as regulations evolve globally.

Strengthens Risk Detection in Real-Time

Traditional periodic KYC checks may miss sudden changes in ownership or suspicious behaviour. With event-driven triggers, pKYC enables early detection of ML/TF risks, ensuring quicker response to potential threats.

Improves Efficiency and Reduces Costs

Manual KYC checks demand extensive time as well as resources. Automation through pKYC reduces this burden, enabling firms to save costs while allowing compliance staff to focus on high-risk cases.

Enhances Customer Trust and Transparency

Customers increasingly expect their Financial Institutions to protect their data and act responsibly. Continuous oversight reassures both regulators and clients, improving reputation while building stronger, long-term customer relationships.

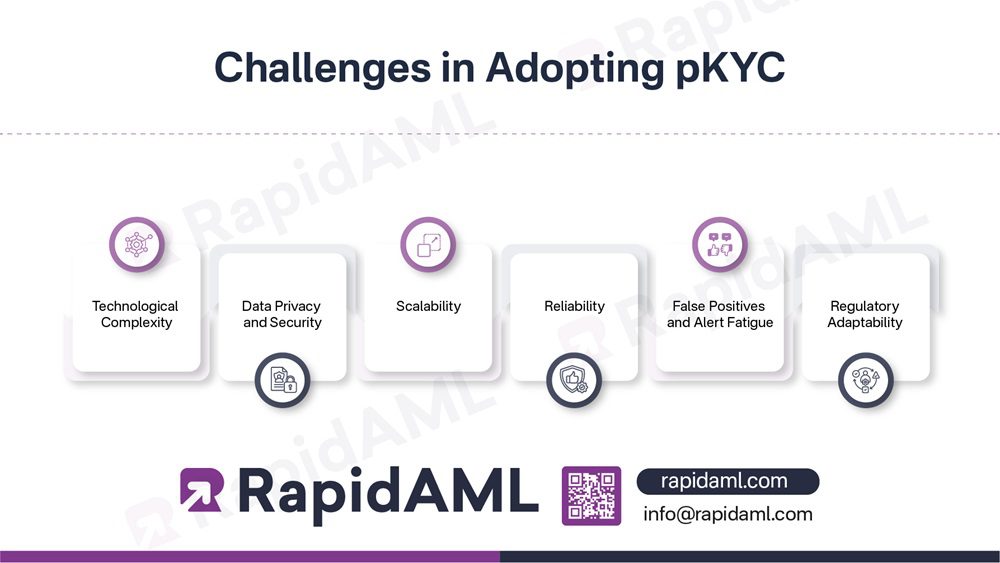

Even though pKYC strengthens the AML/CTF compliance and improves risk management, it comes with several challenges:

Technological Complexity

Setting up pKYC demands advanced systems like Artificial Intelligence (AI), real-time monitoring, and data analytics. Integrating these with existing AML systems or outdated infrastructure is often costly and complex.

Data Privacy and Security

Continuous monitoring involves handling large amounts of sensitive customer data. Institutions must comply with varying privacy laws across jurisdictions while also guarding against cyber threats such as data leaks or hacking.

Scalability

Large Institutions handle millions of records daily. Ensuring real-time updates and monitoring at scale demands strong infrastructure and significant ongoing investment.

Reliability

The success of the pKYC initiative largely depends on the quality of the data available at the central registry and other external sources. Often, customers do not update their data with the central registry, and that undermines the reliability of the data from a risk assessment perspective

False Positives and Alert Fatigue

Automated Transaction Monitoring may generate too many false positives, creating “alert fatigue” for compliance teams and reducing efficiency in spotting genuine risk detection.

Regulatory Adaptability

AML/CTF regulations evolve quickly across jurisdictions. Firms are required to constantly update pKYC frameworks to remain compliant and ensure global consistency.

pKYC is transforming AML compliance by enabling continuous monitoring, automation, and real-time risk management. To implement pKYC effectively, Financial Institutions must adopt structured best practices that balance technology, regulation, and human oversight.

Formulate a Clear pKYC Strategy

A successful pKYC program starts with a defined strategy outlining objectives, automation scope, resources, timelines and workforce training. Institutions must plan migration from manual KYC to automated solutions without creating data silos.

Build a Strong Data Strategy

Data quality is the foundation of pKYC. Institutions must integrate customer information spread across different systems and ensure structured feeds that generate alerts. Without reliable data, automation cannot produce accurate results.

Digitise Workflows for Compliance

Compliance rules should be translated into automated workflows. For instance, the system must be able to direct low-risk cases to Simplified Due Diligence (SDD) while flagging complex ones for enhanced review.

Integrate Monitoring and Alerts

Real-time alerts are vital. A pKYC system should connect with existing AML Software so that any update in customer details, such as a change of address or ownership, automatically triggers a review.

Embed Pre-Onboarding Checks

Regulators also insist that entities perform pre-onboarding checks. Australia has enacted new AML/CFT regulations, which require regulated entities to perform strong pre-onboarding checks before a customer relationship begins. When combined with perpetual screening, this creates a layered defence, mitigating risks at entry level and maintaining vigilance throughout the customer lifecycle.

Balance Automation with Human Oversight

Not all cases can be automated. Analysts should focus on high-risk profiles and false positives. For example, unusual transactions flagged by AI may still need manual investigation to confirm suspicion.

Secure Senior Management Support

Strong leadership sets the tone for compliance. Senior Management should allocate resources, form implementation teams and regularly review the progress of pKYC deployment.

Stay Updated with Regulatory Changes

pKYC systems must evolve with changing laws. Updating risk triggers and thresholds helps ensure continuous compliance. For instance, when the rules are tightened on Beneficial Ownership, institutions must adapt their pKYC settings quickly.

Define KPIs and Measure Effectiveness

Institutions should monitor key indicators such as alert resolution time and false positive rates. Regular feedback from users and customers ensures that the system remains efficient and adaptable over time.

pKYC works best when data, automation, human oversight, and regulatory updates come together. With the right practices, institutions can achieve stronger, more efficient AML compliance.

Conclusion

pKYC strengthens AML compliance by addressing risks that traditional reviews often miss, such as customer profile changes. Though challenges like privacy, integration, and scalability persist, institutions that adopt strong data strategies, digitised workflows, and regulatory adaptability can transform pKYC into a powerful tool for both risk mitigation and building sustainable customer trust.