KYC software plays a crucial role in enabling auditing and accounting professionals to deliver a seamless customer experience and adhere to AML/CFT compliance requirements. Know Your Customer (KYC) Software helps auditors and independent accountants in the UAE to meet the KYC obligations before onboarding customers and establishing a business relationship

What is KYC for Auditors and Independent Accountants in UAE?

Auditors and Independent Accountants in UAE must incorporate the Know Your Customer (KYC) process as a part of their Customer Due Diligence (CDD) obligations to defend against the evolving ML/TF and PF typologies. It is important to understand the CDD first to decode KYC compliance requirements under the UAE’s AML/CFT laws and regulations.

The elements that form the CDD process can be broadly categorised into three categories: KYC, Risk Assessment, and Ongoing Monitoring.

Know Your Customer or KYC, in literal definition, means knowing the potential customer through a systematic process of identifying and verifying details to rule out any criminal intentions or the possibility of illicit financial activity or transactions. As a crucial element of the CDD process, KYC helps determine and mitigate any risks associated with ML/TF/PF and other financial crime activities.

UAE, a financial hub, has stringent AML/CFT regulations, and auditors and independent accountants play a crucial role in maintaining financial integrity, making the KYC process a compliance requirement.

With increasing regulatory oversight and rising compliance risks, a deeper understanding of the KYC obligations of accounting professionals in the UAE is essential. Below are the obligations discussed briefly for better understanding:

The first step auditors and independent accountants must take is to collect customer information details such as:

Regulated entities can make use of KYC software for accountants and automate these compliance processes.

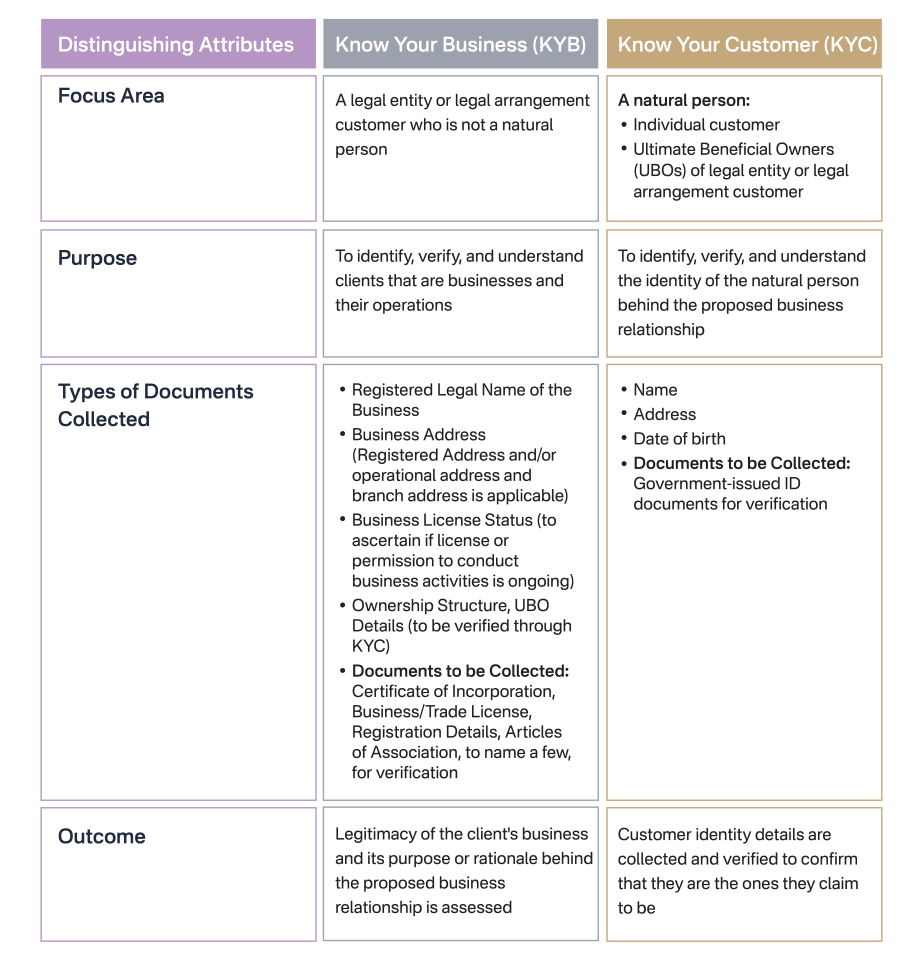

There is a fine line between the KYC (Know Your Customer) process for natural persons and the KYB (Know Your Business) process for legal entities, as a few elements of the two processes are similar. Accounting professionals must recognise these minor differences and take the necessary measures accordingly. The auditors can make use of KYC software to automate these compliance processes.

A detailed understanding of KYB for Auditors and Independent Accountants in UAE includes core elements such as:

Each of these core elements is elaborated below:

For more information about Know Your Business requirements, refer to:

Considering the AML compliance requirements in the UAE, auditors and independent accountants are required to identify and verify the Ultimate Beneficial Owners (UBOs) of a legal entity or a legal arrangement customer. Without UBO identification and verification, the CDD process is considered incomplete and against the compliance norms. KYC software for accounting professionals supports UBO verification, and regulated entities looking to automate their compliance processes implement the ID verification and document verification features of KYC software to ensure their AML/CFT compliance.

The infographic below depicts the criteria for UBO identification in UAE.

After collecting relevant information about the customer, the second step involves verifying the authenticity, validity, and legitimacy of the collected information. Accounting professionals rely on copies of documents such as a passport, Emirates ID, National ID card, driver’s license, utility bills, and bank account details to verify customer information. KYC software for auditors and accountants offers the functionality for customer authentication and ID verification.

Prior to establishing relationships with legal entities, auditors and independent accountants must rule out the possibility of legal entities as a front for ML, FT, and PF activities or, in simpler terms, a shell company. It is necessary for these accounting professionals to have a basic understanding of the difference between a legitimate and a shell company.

CRA involves assessing the ML, FT, and PF risk posed by each customer to auditors and independent accountants on the basis of the following factors:

Once the risk assessment is conducted with appropriate measures, the customers are further classified into low-risk, medium-risk, and high-risk, which further helps to identify the extent and frequency of monitoring required.

Tracking, analysing, and understanding customers' behaviour, as well as account and transaction activities, on a regular basis, is known as ongoing monitoring. This process comes into play only when the customer is assigned to a risk classification to set the frequency and intensity of the monitoring required so that accounting professionals can stay on top of changing information and situations. Many auditors rely on KYC software to ensure that the customers are continuously monitored and flagged for any changes in their profiles and business activities.

As the last step of the CDD process, auditors and independent accountants are required by the AML/CFT regulations in the UAE to maintain records of the methodology, controls in place, and the database built and relied on for KYC purposes.

UAE Mainland authorities for AML/CFT have specified a duration of 5 years to retain and maintain the CDD and other AML/CFT records. The record-keeping requirements for other free zones and financial free zones, such as DIFC or ADGM, are different from those mentioned for the mainland. KYC software for Chartered Accountants helps maintain customer documents and comply with mandatory record-keeping obligations.

Learn more about AML/CFT Record-Keeping obligations in the UAE by referring to:

Take a glance at the compliance requirements depicted in the infographic on the Know Your Customer (KYC) Process flow for auditors and independent accountants in the UAE, to understand the importance of effective KYC.

The following factors state how effective KYC is a non-negotiable AML/CFT and TFS Compliance requirement:

An effective KYC process and equally efficient AML software are correlated, as the results directly impact the quality and accuracy of CDD measures and improve the accuracy of sanctions compliance.

Effective KYC helps auditors and independent accountants obtain accurate customer details, which can be used to conduct sanctions screening exercises accurately and adhere to AML/CFT compliance requirements. Error-free and consistent KYC helps ensure a seamless CDD journey for the business and clients.

Effective KYC enables the AML compliance officer to file regulatory reports such as SAR and STR in a timely manner through the goAML portal and within the prescribed timeframe.

Refer to Suspicious Activity Reporting (SAR) for DNFBPs and VASPs, An Ultimate Guide to Investigating Suspicious Transactions, and Transforming Suspicious Transaction Reporting with AI to understand regulatory reporting requirements in the UAE.

Efficient KYC, usually conducted by a KYC Analyst, helps with the commencement of CRA and adequate adopting due diligence measures, helping the AML compliance officer delegate tasks to the AML compliance team, such as assigning CRA to a Risk Analyst, sanctions screening to a Screening Analyst, ongoing monitoring to the Transaction Monitoring Analyst, as the situation demands. An efficient KYC process implemented in the KYC software helps accounting professionals accelerate their AML compliance workflow.

Customer experience plays a significant role in ensuring the growth and development of any entity, and an effective KYC promotes customer experience by further simplifying the process of verification, timely onboarding of customers, and compliance without unnecessary friction.

Additionally, effective KYC helps with customer data privacy by securely storing verified information and tailoring services based on customer profiles. This improves trust and legitimacy, making the customer experience smoother and more reliable due to data privacy and security.

Enhancing Customer Experience and Ensuring KYC Compliance for detailed insights.

Implementing the KYC process presents its own set of challenges.

These challenges can be classified into three categories: challenges faced during manual KYC, challenges faced using a hybrid or automated KYC tool, and some of the common pain points.

1. Manual KYC process, also known as the traditional KYC process, when opted for, has operational pain points as discussed below:

Manual KYC, officially known as Traditional KYC, requires KYC analysts to manually collect, enter, and verify customer information using physical documents and government IDs. Comparing the collected documents with originals and checking for authenticity against the official database is tedious and time-consuming. This manual process of performing KYC leads to the following pain points:

As established earlier, there are several factors of manual KYC, from document collection to data entry into KYC forms and questionnaires, that need to be performed, which end up consuming a significant number of man-hours, eventually draining resources as well as productivity. KYC software for accountants will help overcome this bottleneck.

When a customer is not available in person for identity and document verification, the manual KYC process becomes more vulnerable to risks of identity theft, spoofing, or impersonation. Verifying customer details remotely can result in high-risk consequences.

One of the challenges of the manual KYC process is that it is heavily reliant on humans performing repetitive tasks, resulting in an increase in human errors, such as:

Also, when human-driven processes do not have adequate checks and balances, the risk of such a process becoming prone to fraud increases drastically.

2. Operational Pain Points faced by auditors and independent accountants while relying on hybrid, legacy, as well as KYC Automation tools:

Auditors and independent accountants, when relying on automated KYC software, aim to achieve accurate and faster results of KYC compliance. However, these accounting professionals should consider the operational issues posed by relying on eKYC software, as mentioned below:

The KYC software in the UAE’s automation market has a wide range of options.However, a majority of them lack flexibility and adaptability, forcing auditors and independent accountants to adapt their workflows to legacy or rigid software structures. This hampers efficiency and increases human or manual interventions.

Read MoreIn today’s world, a rise in AI-generated manipulations, including deepfakes, poses challenges in verifying identities and checking for authenticity. This, in turn,

makes accounting professionals navigate through additional layers of validation, making the KYC process more complicated than it is.

With the use of technology, the risk of Cyber-Enabled Fraud (CEF) is bound to impact KYC software and eKYC tools. Examples of emerging CEF include the abuse of deepfakes and generative AI, which are used to commit fraud by impersonating and circumventing biometric checks by creating deepfakes of a person’s voice and video. These deepfakes are used to circumvent liveness checks to commit account takeover fraud.

Due to a huge gap between legacy or hybrid systems and modern compliance tools, accounting professionals’ KYC process experience is no longer smooth and seamless. This integration issue leads to broken or fragmented data, elements of inefficiency, and a higher risk of errors or misinterpretations.

Read MoreThe KYC process is about collecting sensitive customer information and managing such personal and financial data, which requires robust privacy and security frameworks. However, many KYC automation tools available on the market either lack strong encryption or compliance mechanisms, making customer data vulnerable to breaches and exposing accounting professionals to regulatory penalties.

Read More

As per AML/CFT compliance requirements, auditors and independent accountants are required to conduct KYC for occasional customers once. However, for ongoing business relationships, the KYC should be conducted periodically, based on the risk scoring assigned to them. If accounting professionals neglect the KYC refresh requirement, it is considered non-compliant behaviour.

AML/CFT regulations are prone to updates, and if auditors and independent accountants fail to keep up with the changing regulatory requirements by following outdated methodologies for the KYC process, this might lead to non-compliance or inadequate measures.

Auditors and independent accountants often struggle with implementing monitoring measures due to an unclear distinction between occasional and ongoing business relationships, making AML/CFT compliance difficult.

KYC implementation, whether manual, hybrid, or software/tool-based, demands an investment of resources and finances. Limited funds for AML compliance make it difficult for accounting professionals to meet the requirements accurately and efficiently.

Auditors and independent accountants in the UAE must comply with both domestic AML/CFT laws and regulations of customers’ home countries. Particularly, those having branch offices or group entities in multiple jurisdictions require developing standard and uniform AML/CFT compliance measures for the KYC process, which is a navigational pain point for accounting professionals.

While attempting to understand and analyse the KYC process, the first step is to identify the pain points in such a KYC process, and the next step is to have an overview of the consequences or the intensity of impact it will have on the business.

The auditors and independent accountants must follow the same approach to understand the KYC challenges and their impact on their day-to-day functions.

When relying on manual, traditional, or legacy models for fulfilling KYC obligations, customer onboarding is bound to get delayed due to the involvement of human factor, i.e., the AML compliance team, as its productivity is exhausted in completing time-consuming, repetitive tasks of filling out KYC forms and questionnaires, while maintaining KYC registers for accounting professionals.

Delayed customer onboarding, coupled with a traditional tick-box approach, results in increased compliance costs. Independent accountants and auditors are unable to deploy simplified due diligence measures on customers where ML/FT and PF risks are low.

Compliance costs also increase due to poorly customised KYC forms and questionnaires, where KYC Analysts and customers end up spending time filling out materially irrelevant or insignificant information. Learn more about AML Non-Compliance: An Unaffordable Cost.

Tick-box-based KYC measures that are devoid of RBA and neglect regulatory requirements, such as KYC refresh, leading accounting professionals towards grave consequences of non-compliance, fines, and penalties. Independent accountants and auditors in the UAE face an extreme cost burden and reputational damage due to violations of AML/CFT regulations.

When the KYC process is time-consuming and delays the customer onboarding timeline, AML compliance teams, particularly KYC and Screening Analysts, rush the process, leading to errors and hindering risk-based CDD implementation.

Independent accountants and auditors follow and rely on a tick-box approach that often fails to assess customer risks accurately, leading to compliance violations and penalties.

Acknowledging the fact that an inaccurate KYC process may directly pose higher ML/TF and PF risks is like calling a spade a spade. Poor AML/CFT controls expose accounting professionals to financial crime risks. Weak measures fail to tackle multi-jurisdictional compliance, data privacy, and monitoring challenges.

Refer:

Don’t Let KYC Delays Cost You and Your Productivity

Discover How to Fix Delays and Reduce Risk

RapidAML, with its KYC automation feature, makes it simple for auditors and independent accountants to comply with KYC requirements. This simplification of the KYC process takes place in 8 steps, as elaborated.

Leveraging Technological Solutions

RapidAML integrates AI-powered automation and machine learning to streamline compliance-adhering processes. With the best of both worlds from the technological expertise of RapidAML’s makers and AML Compliance expertise from their knowledge partner – NIYEAHMA, RapidAML’s KYC Software for Auditors and Accountants in UAE aims to achieve systematic yet automated analysis and maintenance of customer information.

Customer Identification and Verification Tools

With RapidAML’s centralised dashboard, KYC analysts of accounting professionals can efficiently manage customer identification and verification. Through the one-stop solution of the dashboard, the eKYC tool enables smooth navigation and easier review of individual or linked entities’ profiles and verifies uploaded documents seamlessly.

Document Authentication and Verification Systems

With features like accurate verification systems for document validation, KYC Software from RapidAML enables accounting professionals to integrate the customer onboarding process with UAE PASS to verify their customers’ identities and offers a seamless customer onboarding experience.

Secure Electronic Platforms

RapidAML’s KYC Software, to mitigate cyber-enabled fraud (CEF) risks, facilitates 2-factor authentication (2FA) for accessing and validating customer profiles. The 2FA component makes it difficult for fraudsters and financial criminals to misuse customer information stored and entered on the RapidAML platform.

Optimising Customer Onboarding

RapidAML’s KYC software comes with a KYC self-service option. KYC self-service simplifies customer onboarding while ensuring strict regulatory compliance. It facilitates KYC declarations through an OTP-based authentication process, creating a secure customer identity verification environment while improving efficiency.

Simplifying KYC Forms

One of the standout features of RapidAML is its customisable KYC questionnaires or templates, enabling auditors and independent accountants to create tailor-made KYC forms as per their business needs. RapidAML, with its library of pre-built templates, offers accounting professionals a wide range of options to create standard or adaptive KYC forms.

Utilising Pre-Filled KYC Forms with Third-Party Integrations

RapidAML KYC software can integrate with third-party solutions to capture information to generate pre-filled KYC forms, reducing the duplication effort and saving time and costs.

Offering Multiple Channels for Onboarding

With the option to choose from multiple channels, RapidAML enables auditors and independent accountants to obtain customer information through Self-KYC functionality, which can be accessed by customers through their mobile phones.

Learn more about KYC Automation Strategies in UAE

Refer to: Why is eKYC a Game-Changer?

See How RapidAML Solve Your KYC Burdens

Stay Compliant, While Saving Your Cost, Effort and Time

RapidAML KYC Software, with its advanced technology, helps keep an eagle-eye view while performing KYC, working hand-in-hand with the UAE’s AML/CFT and TFS obligations applicable to auditors and independent accountants.

For a better understanding, take a look at the distinct features of RapidAML that help resolve KYC-related issues faced by auditors and independent accountants in the UAE.

RapidAML KYC: Smart Fit for UAE Accountants and Auditors

From a multi-organisational perspective, RapidAML enables auditors and independent accountants to add as many users as necessary, ensuring that it promotes a multi-organisation environment where KYC templates can be applied uniformly, ultimately making KYC compliance scalable.

RapidAML stands out by simplifying the KYC process at every step, making sure that auditors and independent accountants comply with UAE AML/CFT regulations. This KYC software is developed using state-of-the-art technology and provides faster and easier solutions.

Who said it is tedious to get all the information from diverse sources in one place? With RapidAML’s efficient integration capabilities and built-in template library and workflows, any accounting professional can implement and operate in the shortest possible time. This KYC software can integrate seamlessly with ERP and POS systems, which automates business processes.

RapidAML KYC software’s team is not only equipped to resolve KYC software-related issues faced while using the RapidAML KYC software but also provides valuable insights regarding establishing a watertight KYC/KYB process for auditors and accounting professionals that also addresses components such as:

1. KYC Training and Awareness

2. KYC/KYB Software Implementation

3. KYC/KYB Questionnaire

4. KYC/KYB Policies and Procedures

5. AML/CFT/CPF Program

RapidAML KYC software is not just about easing the KYC process for accounting professionals; it also promotes and enhances customer experience through proven strategies as mentioned below:

1. Ensuring Data Privacy and Security

2. Using Self KYC Functionality

3. Conducting Adequate Reviews and Audits

4. Ensuring Timely Communication

5. Providing Adequate KYC Support and Guidance

6. Adopting a Risk-Based Approach

Learn more about Enhancing Customer Experience and Ensuring KYC Compliance.

RapidAML’s Kanban board is a one-stop solution that helps auditors and independent accountants with the ease of locating customer case files, staying on top of document expiry dates, and checking the onboarding status of their prospective customers on a single screen.

As it comes with a user-friendly interface, the KYC software eliminates the endless navigation in the Contact Register as well as the KYC register. This helps accounting professionals, KYC analysts and AML Compliance Officers with a 360-degree analysis of a customer’s profile.

RapidAML is not about ‘one size fits all’ ideology and offers KYC templates that can be tailored as per business needs. This KYC software for auditors has a wide range of customisable templates and also has a functionality to select role-wise accessibility to complete KYC checks, as well as self-KYC verification.

For better functioning and meeting the operational needs of auditors and independent accountants, RapidAML KYC software comes with the function of easy access and download of various reports. Reports such as contact lists, KYC lists for individuals and legal entities, and customer account registers of active, dormant, inactive, and exited customers can all be available with just one click.

These reports and registers help accounting professionals identify the origin of their ML, FT, and PF risks emanating from their customers. Also, the information contained in these registers helps with writing details for SAR/STR and other regulatory reports’ narratives whenever any suspicious element is discovered and warrants regulatory reporting. These reports also help in re-evaluating Enterprise-Wide Risk Assessment (EWRA).

With a self-KYC functionality that offers features like obtaining consent through an electronic signature, RapidAML KYC software is designed to ease customer onboarding remotely while keeping compliance requirements as a priority.

Refer to our blog for more information on Remote Customer Onboarding and ML/TF Risk Mitigation.

As the KYC process is about collecting, identifying, and verifying customer details through documents, RapidAML KYC software facilitates verification and authentication features by relying on government-approved databases.

The previously discussed feature of downloadable reports plays a crucial role in acting as documentary evidence, helping auditors and independent accountants establish an effective and accurate audit trail. This audit trail is essential in both internal and external independent AML audits. Further, RapidAML KYC software for accountants and auditors logs each and every action performed by the user to ensure that it knows who did what and when.

In today’s world, storing and navigating files and reports on a computer’s local drive is considered prehistoric human behaviour - it is outdated and tedious.

For efficient use of RapidAML, an internet connection and access to a laptop/computer are all that is needed, as a cloud-based KYC software enables auditors and independent accountants to store, navigate, and access any file with a simple click from anywhere.

RapidAML KYC software is built on strong foundations in information privacy and cybersecurity, making it a robust software that any accounting professional can rely on without thinking twice.

As data security and privacy protocols are embedded into the KYC software at the software design and development stage, adequate compliance with these requirements is an obvious outcome during the course of its normal use.

RapidAML KYC software helps auditors and independent accountants in the UAE to implement RBA through its KYC automation software, as it helps with the risk-centric configuration of re-KYC through the risk-scoring assigned, configuring re-KYC triggers and generating timely notifications for KYC document expiry and re-KYC.

RapidAML KYC software efficiently identifies any changes in customer information, such as when a KYC document expires. It triggers alerts and notifications to accounting professionals and outlines the next steps to be taken. This KYC software aids auditors and independent accountants in conducting effective ongoing monitoring of their business relationships.

To take a path for an efficient yet successful implementation of KYC software, auditors and independent accountants must showcase precision, adhere to compliance norms, and execute seamlessly, all while being within the boundaries of regulatory requirements.

The best practices to achieve a successful implementation of KYC software are as follows:

Auditors and independent accountants in the UAE must opt for KYC software that is well-suited to identify and verify customer information and support different business requirements while adhering to AML/CFT compliance measures.

The KYC software should align well with the latest EWRA standards and adhere to TFS regulations while promoting a business perspective and growth. This further helps accounting professionals to customise templates to cover key fields for obtaining accurate information from customers and performing Customer Risk Assessment, which helps conclude risk-based CDD obligations.

For a seamless migration from a manual or traditional KYC process or a different KYC software to RapidAML KYC software, auditors and independent accountants must understand and analyse the KYC requirements before initiating the migration phase.

It is crucial to understand the prerequisites of migration in order for auditors and independent accountants to prepare or modify existing customer data and files in a format that will be supported by the new KYC software without any errors or inefficiencies. Any misalignment with data requirements may result in severe consequences, such as loss of data, leading to a breach of record-keeping requirements, business, or reputational loss.

When opting for KYC software prior to migrating crucial data and information, it is essential to consider a KYC software that facilitates hassle-free data migration to avoid any consequences of non-compliance.

Just as test-driving a car before buying to make sure everything works well, test-driving the KYC software is a must. This makes an accounting professional open to identifying features of KYC software that need fine-tuning or customisation to meet business needs.

For instance, auditors and independent accountants must test the software to look for missed notifications when a document expires, check for any loose ends within the workflow, and identify any technical glitches. This makes the KYC software run efficiently and smoothens the KYC journey of any customer.

Additionally, accounting professionals must not miss out on documenting these KYC software protocols, KYC templates, questionnaires relied upon, re-KYC timelines followed and simplified as well as enhanced due diligence thresholds within their AML/CFT and CPF Policies, Procedures, and Controls, forming part of the AML/CFT and CPF Program.

Conducting KYC is not just a safety measure but a pivotal start of an effective compliance journey for auditors and independent accountants, as well as potential and existing customers. An effective KYC process leads to an accurate screening, CRA and reporting process. By being a strong barrier against ML, FT & PF risks, KYC software safeguards the entity by identifying and verifying the authenticity of its customers and documents received to highlight any red flags to accounting professionals, KYC analysts and AML Compliance Officers.

Auditors and independent accountants, while ensuring long-term efficiency, must assess the cost-benefit ratio and select a KYC software that minimises risks and manual intervention with better and easier functionality.

Auditors and independent accountants who clearly define the capabilities of each user, outline a hierarchy escalation matrix, and accurately map workflows, making the KYC software work efficiently for them.

To achieve the smooth implementation of defining users and their roles, accounting professionals can reach out to vendor support for assistance in a seamless transition and bridge any gaps through training and awareness sessions.

In order to ensure the successful implementation of KYC software, it is crucial for auditors and independent accountants to define a methodology for UBO identification and verification through the KYC software that is in alignment with AML compliance requirements.

These accounting professionals must develop a methodology to ensure that they link UBOs with their respective legal entities, derive a holistic CRA of business entities, in order to establish a business relationship, and further implement risk-centred CDD measures.

Refer to A Guide for UBO Compliance for DNFBPs in UAE to learn more about UBO compliance in UAE.

Configuring alerts, notifications, and task completion timelines is an action item for auditors and independent accountants, which, when combined with efficient KYC software, can help accounting professionals achieve all-rounded AML/CFT compliance excellence.

Integration functionality in KYC software helps accounting professionals minimise operational costs and reduce overlapping efforts. It should integrate with other existing AML software and tools to aid accounting professionals in streamlining AML compliance requirements, such as sanctions screening, CRA, EWRA, and ongoing monitoring under a single tool.

Auditors and independent accountants must continuously assess the post-implementation outcomes to analyse the cause of the success or failure of the KYC software. This helps ensure alignment with organisational goals for compliance at all times.

Assessment of post-implementation outcomes also helps identify and analyse whether to continue using the same KYC software during business expansion or to look for alternatives. This analysis makes it easier for accounting professionals by having ongoing viability tests of the KYC software, ensuring compliance and operational success.

To match the ever-evolving nature of regulatory requirements, business needs, changes in the FATF grey or black lists, or sanction regimes, auditors and independent accountants must re-tune or reconfigure screening tools.

The configuration adaptations help auditors and independent accountants better defend against threats and ensure no lag in compliance measures. To promote transparency and easy accessibility, these adaptations should be reflected in the AML/CFT policies and procedures as a compliance protocol to reduce audit queries and regulatory scrutiny.

Excel KYC Software Implementation with Confidence

Discover Key Steps to Handle Your KYC System

In a fast-changing regulatory environment, auditors and independent accountants in the UAE require effective and robust compliance solutions. RapidAML is a torchbearer in devising KYC software that takes the burden off accounting professionals’ shoulders and leads the way towards effective implementation of AML/CFT and TFS compliance requirements, particularly in meeting the screening obligations in the UAE.

Name Screening Software for Auditors and Independent Accountants in UAE <img src="https://rapidaml.com/wp-content/uploads/2025/05/UAE_flag.svg">

Name Screening Software for Auditors and Independent Accountants in Australia <img src="https://rapidaml.com/wp-content/uploads/2025/05/Australia_flag.svg">

Name Screening Software for Auditors and Independent Accountants in UK <img src="https://rapidaml.com/wp-content/uploads/2025/05/UK_flag.svg">

Name Screening Software for Auditors and Independent Accountants in Singapore <img src="https://rapidaml.com/wp-content/uploads/2025/05/Singapore_flag.svg">

Name Screening Software for Auditors and Independent Accountants in India <img src="https://rapidaml.com/wp-content/uploads/2025/05/India_flag.svg">

KYC Software for Auditors and Independent Accountants in UAE <img src="https://rapidaml.com/wp-content/uploads/2025/05/UAE_flag.svg" >

KYC Software for Auditors and Independent Accountants in Australia <img src="https://rapidaml.com/wp-content/uploads/2025/05/Australia_flag.svg">

KYC Software for Auditors and Independent Accountants in UK <img src="https://rapidaml.com/wp-content/uploads/2025/05/UK_flag.svg">

KYC Software for Auditors and Independent Accountants in Singapore <img src="https://rapidaml.com/wp-content/uploads/2025/05/Singapore_flag.svg">

KYC Software for Auditors and Independent Accountants in India <img src="https://rapidaml.com/wp-content/uploads/2025/05/India_flag.svg">

CRA Software for Auditors and Independent Accountants in UAE <img src="https://rapidaml.com/wp-content/uploads/2025/05/UAE_flag.svg" >

CRA Software for Auditors and Independent Accountants in Australia <img src="https://rapidaml.com/wp-content/uploads/2025/05/Australia_flag.svg">

CRA Software for Auditors and Independent Accountants in UK <img src="https://rapidaml.com/wp-content/uploads/2025/05/UK_flag.svg">

CRA Software for Auditors and Independent Accountants in Singapore <img src="https://rapidaml.com/wp-content/uploads/2025/05/Singapore_flag.svg">

CRA Software for Auditors and Independent Accountants in India <img src="https://rapidaml.com/wp-content/uploads/2025/05/India_flag.svg">

Transaction Monitoring Software for Auditors and Independent Accountants in UAE <img src="https://rapidaml.com/wp-content/uploads/2025/05/UAE_flag.svg" >

Transaction Monitoring Software for Auditors and Independent Accountants in Australia <img src="https://rapidaml.com/wp-content/uploads/2025/05/Australia_flag.svg">

Transaction Monitoring Software for Auditors and Independent Accountants in UK <img src="https://rapidaml.com/wp-content/uploads/2025/05/UK_flag.svg">

Transaction Monitoring Software for Auditors and Independent Accountants in Singapore <img src="https://rapidaml.com/wp-content/uploads/2025/05/Singapore_flag.svg">

Transaction Monitoring Software for Auditors and Independent Accountants in India <img src="https://rapidaml.com/wp-content/uploads/2025/05/India_flag.svg">

EWRA Software for Auditors and Independent Accountants in UAE <img src="https://rapidaml.com/wp-content/uploads/2025/05/UAE_flag.svg" >

EWRA Software for Auditors and Independent Accountants in Australia <img src="https://rapidaml.com/wp-content/uploads/2025/05/Australia_flag.svg">

EWRA Software for Auditors and Independent Accountants in UK <img src="https://rapidaml.com/wp-content/uploads/2025/05/UK_flag.svg">

EWRA Software for Auditors and Independent Accountants in Singapore <img src="https://rapidaml.com/wp-content/uploads/2025/05/Singapore_flag.svg">

EWRA Software for Auditors and Independent Accountants in India <img src="https://rapidaml.com/wp-content/uploads/2025/05/India_flag.svg">

Regulatory Reporting Software for Auditors and Independent Accountantss in UAE <img src="https://rapidaml.com/wp-content/uploads/2025/05/UAE_flag.svg" >

Regulatory Reporting for Auditors and Independent Accountants in Australia <img src="https://rapidaml.com/wp-content/uploads/2025/05/Australia_flag.svg">

Regulatory Reporting Software for Auditors and Independent Accountants in UK <img src="https://rapidaml.com/wp-content/uploads/2025/05/UK_flag.svg">

Regulatory Reporting Software for Auditors and Independent Accountants in Singapore <img src="https://rapidaml.com/wp-content/uploads/2025/05/Singapore_flag.svg">

Regulatory Reporting Software for Auditors and Independent Accountantss in India <img src="https://rapidaml.com/wp-content/uploads/2025/05/India_flag.svg">

Case Management Software for Auditors and Independent Accountants in UAE <img src="https://rapidaml.com/wp-content/uploads/2025/05/UAE_flag.svg" >

Case Management for Auditors and Independent Accountants in Australia <img src="https://rapidaml.com/wp-content/uploads/2025/05/Australia_flag.svg">

Case Management Software for Auditors and Independent Accountants in UK <img src="https://rapidaml.com/wp-content/uploads/2025/05/UK_flag.svg">

Case Management Software for Auditors and Independent Accountants in Singapore <img src="https://rapidaml.com/wp-content/uploads/2025/05/Singapore_flag.svg">

Case Management Software for Auditors and Independent Accountants in India <img src="https://rapidaml.com/wp-content/uploads/2025/05/India_flag.svg">

Get Started

Contact Us